In recent months there have been a number of interesting developments in global asset markets. In general it's all good news: the dollar is strengthening, gold is teetering, interest rates are rising, commodities are resilient, equities are rising, credit spreads are narrowing, and emerging markets are recovering. Not everything is rosy, however, but on balance the market's message is that global economic growth is expected to improve for the foreseeable future, while inflation is likely to remain relatively low and stable.

I continue to believe that there is a lot of

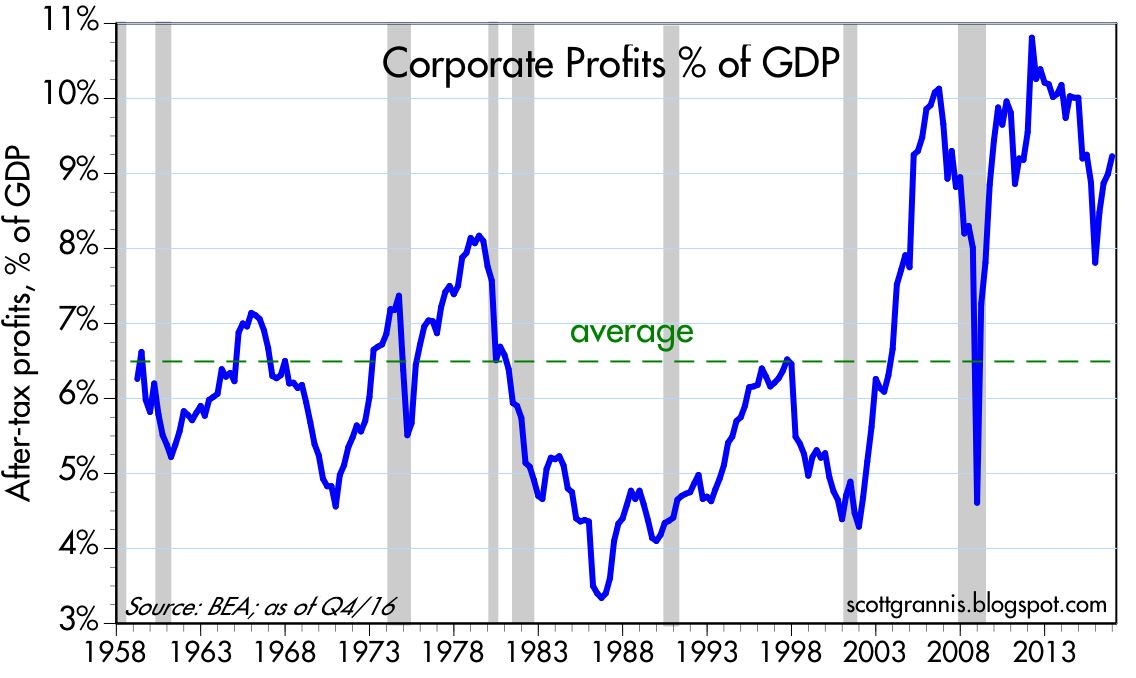

upside potential in the U.S. economy, and I that the outlook for corporate profits is improving now that oil prices are no longer declining and confidence is on the rise. What's changed to make all this possible? The direction of policy: after years or moving in the wrong direction, regulatory burdens going forward are likely to decline, marginal tax rates are likely to decline, the U.S. tax code is likely to be simplified, and markets are likely to become freer and fairer. Trump may not do everything right, but as long as he fixes at least a few things, we'll be better off in the future than we have been in the past.

From my supply-side perspective, this means that the incentives to work, invest, and take risk are on the cusp of rising, and so in coming years we are likely to see more people looking for work, more jobs being created, stronger productivity gains, and expanding trade and prosperity globally. It's hard to say how much improvement there will actually be, but the important thing is that

on the margin, things are likely to improve. That's what moves markets: the direction of change on the margin relative to expectations for change.

Here are 20+ charts that tell the story:

The value of the dollar is arguably one of the most important financial variables, since it is effectively the price of admission to the world's biggest, wealthiest, and most influential economy. A rising dollar is thus a good sign that the world is more interested in gaining exposure to our economy, and that in turn means more investment and more growth—it's a virtuous cycle. The chart above is arguably the best measure of the dollar's value vis a vis other currencies, since it is calculated on a trade-weighted, inflation-adjusted basis. It was only a few years ago that the dollar was scraping the bottom of the barrel, trading at all-time lows. Back then it was far from clear whether the U.S. would ever recover its former glory, or ever manage to grow by more than 2% a year. Today, in contrast, animal spirits are making a comeback. Hope is returning.

Today's ADP employment report, which far exceeded expectations, was at least a partial sign of a revival in animal spirits. But as the chart above shows, we have seen quite a few spikes like this in prior years, only to have them reversed in subsequent months. In other words, it's too early to be confident in a significant and lasting pickup in hiring. Nevertheless, since this report comes on the heels of a very strong jump in Small Business Optimism (second chart above), it is reasonable to be optimistic.

History tells us that the value of the dollar and the price of commodities tend to move in opposite directions (see chart above, which compares commodity prices to the inverse of the dollar's value). It's rare that commodity prices should be as strong as they are today given the dollar's impressive rise in recent years. I continue to believe that this signals that a stronger dollar is a harbinger of a stronger U.S. economy and a stronger global economy, and that is what is keeping commodity prices resilient.

Credit Default Swap spreads, shown in the chart above, are a highly liquid market that is an excellent proxy for the market's outlook for corporate creditworthiness. Spreads today are as low as they have been for many years, but they are not yet at the rock-bottom lows we saw in the late 1980s. The message is simple: the market is not very worried about creditworthiness, presumably because the outlook for the economy has improved and there are as yet no signs of deterioration. If there's anything to worry about, it's that spreads are relatively narrow, and that is a sign of optimism. And when optimism is high the market becomes vulnerable to anything that is not good news.

Swap spreads, shown in the chart above, are a unique form of credit spread because they reflect both the health and the liquidity of the financial markets and they are often good leading indicators of the health of the economy. Swap spreads are the market's way of charging for generic risk when entering into large and complex financial transactions with major financial participants. That swap spreads both here and in the Eurozone are rising is therefore a reason to worry. I hasten to note, however, that U.S. swaps spreads, currently about 30 bps, are still within a "normal" range, which would be 20-30 bps. The time to worry is when swap spreads exceed 50-60 bps. Unfortunately, Eurozone swap spreads are now in the worry zone. I think this probably reflects rising concerns in Europe that the French government may decide to exit the EU (i.e., "Frexit"), and if they do, this could pose significant systemic risk for Eurozone financial markets. I note in that regard that 5-yr CDS spreads on French government bonds have spiked to 60-70 bps in recent months, while German government CDS spreads remain relatively benign. In short, markets are worried that the French could do something "stupid" that might in turn lead to defaulting on its obligations. This bears watching, but it's not yet a reason to panic. The world started to panic over Brexit, but since then it has proven to be more a development that is more salutary than concerning.

The chart above compares swap spreads with the spread on high yield corporate debt. Here we see an anomaly: swap spreads are rising while HY spreads are declining. This could be one of those times when swap spreads are the leading indicator for where the rest of credit spreads are headed. For the time being, however, I am more persuaded by the fact that swap spreads are still pretty normal at current levels, so their recent rise is more in the nature of a return to normalcy than it is to the beginnings of deterioration. If they continue to rise in a meaningful fashion, then I'll start to worry that other credit spreads might rise, and the outlook for the economy would therefore deteriorate.

In the two charts above, we see that Commercial and Industrial Loan growth has slowed down significantly in the past four months, after growing at heady, double-digit rates for years. Is this a cause for concern, or is it simply a return to more normal conditions? A slowdown in loan growth is symptomatic of an increase in the demand for money (because wanting money is the opposite of borrowing money). As such, this may well be a healthy development; banks are not lending willy-nilly, and neither are companies borrowing with abandon. It's also important to remember that lending activity does not necessarily drive economic growth; lending can facilitate growth, but it can't create growth out of thin air. Confidence and investment are the keys to growth, and a slowdown in lending activity could be simply a sign of returning confidence. Meanwhile, we know that there is no shortage of money in the system.

The two charts above suggest that bank lending is on solid ground, at least for now. Delinquency rates for both C&I Loans and all bank loans and leases are historically low. To be sure, delinquency rates are more of a coincident than a leading indicator, since companies typically have problems paying off their debts when the economy is deteriorating or very weak. In other words, recessions are not caused by loan defaults; loan defaults are the result of recessions. In any event, these charts tip the scales in favor of rational lending and borrowing behavior.

The chart above has fascinated me for years, since it shows that the prices of TIPS and golds have been highly correlated (the blue line is the inverse of the real yield on TIPS, which is a good proxy for their price). Both of these disparate assets are moving together: how to explain? My best guess is that they share one key attribute, which is "safety." Gold is a classic refuge from uncertainty, and TIPS are not only default-free but government-guaranteed to protect against inflation. That both appear to be declining on the margin suggests that financial markets are becoming somewhat less risk-averse, presumably because the outlook for growth is improving. If the economy becomes healthier, there is less reason for the Fed to take outsize risks, and thus there is less risk of inflation and less risk of a debasement of the dollar. I'd like to see both assets continue to decline in price.

The chart above compares the real and nominal yield on 10-yr Treasuries, with the spread between the two being the equivalent of the market's expected annual rate of inflation over the next 10 years. Inflation expectations have been "anchored" around 2% for several months now, even as yields have reached new highs for the year. This in turn suggests that it is real rates that are driving all rates higher, which implies that rates are rising because the market's growth expectations are rising (real rates typically rise as economic growth picks up). The rise in real rates is still quite modest, however, but it is encouraging and I would expect to see more of the same in the months to come.

One reason the dollar is stronger these days is that other currencies have become less attractive (see charts above). Both the Euro and Sterling are now trading "cheap" relative to my estimate of their Purchasing Power Parity vis a vis the dollar. The dollar is not worth more because the Fed has created a shortage of dollars (which would be deflationary); it is worth more because other currencies are worth less. For that reason I doubt that the dollar's strength is a harbinger of rising deflation risk. It's one more sign that the U.S. economy is attracting the world's capital, and that capital can in turn fuel more investment and growth in the years to come.

The chart above shows that a rising dollar can often be a precursor of rising productivity, and vice versa. I think that puts meat on my argument above: if today's stronger dollar is the result of investment inflows, that in turn suggests that we will see rising productivity—and rising prosperity—in the years to come. Very good news.

Peter Navarro, Trump's trade guru, needs to look at these charts before he leads the U.S. into a trade war with China. Contrary to what he thinks (and he's most assuredly

wrong on almost everything he says), China has not been keeping its currency artificially weak. As the second chart shows, the Chinese yuan has actually appreciated strongly against the currencies of its trading partners on an inflation-adjusted basis. As the first chart shows, the Chinese central bank was a huge buyer of foreign currency from 1995 through 2014 (accumulating some $4 trillion in forex reserves in the process), yet the yuan was continually appreciating over that same period. If they hadn't bought all that incoming foreign capital, the yuan would have appreciated much more than it did. Things have changed a lot in recent years, however. The Chinese central bank has sold $1 trillion of its forex reserves, yet the currency has depreciated. They been trying to prop up the yuan (by selling assets), but the yuan has nevertheless declined. The fact that their forex reserves have been relatively stable for the past several months suggests that the yuan may have found a new equilibrium. In any event, the yuan is still plenty strong, and even though the economy is only growing 6-7% these days (instead of 10%) it is still relatively impressive when you consider the meager growth of the world's developed economies.

The charts above tell a simple story: the outlook for the U.S. economy has brighter than the outlook for the Eurozone or the Japanese economy in recent years. U.S. stocks are at new highs, but the same can not be said for most other countries.

Finally, a quick look at my favorite Latin American economy, Argentina. These charts are very encouraging, since they show that by liberalizing its currency market and respecting its debts, Argentina has regained a good portion of the world's confidence that it had previously lost. Since abandoning its peso peg in December 2015, the peso on the open market has declined only marginally, even though inflation continues to hover in the 25-30% range. More importantly, the central bank has rebuilt Argentina's foreign exchange reserves dramatically over the past year. This further suggests that we ought to see declining inflation—finally—in Argentina in the years to come. Why? Because the relatively stable peso and the huge surge in Argentina's forex reserves are symptomatic of a big increase in the demand for pesos. So even though currency in circulation has expanded by almost 30% in the past year, its safe to say that the demand for those pesos has also increased significantly. And that means that rapid money growth won't be so inflationary going forward as it has been in the past.