Housing prices have been rising for almost four years now, and they were up over 5% nationwide in the year ending last November.

New home sales continue to rise, and probably have a lot of upside left.

Housing starts are likely to continue rising, as suggested by relatively strong builder sentiment and rising building permits. The housing sector is one of the economy's strongest.

As the chart above shows, new applications for home mortgages (not including refis) are up 40% from the levels that prevailed during 2014. 30-yr fixed conforming mortgage rates currently are 3.7%, and with the exception of 10 months in late 2012 and early 2013, have never been lower. If confidence continues to improve, there is every reason to think the housing market has plenty of upside.

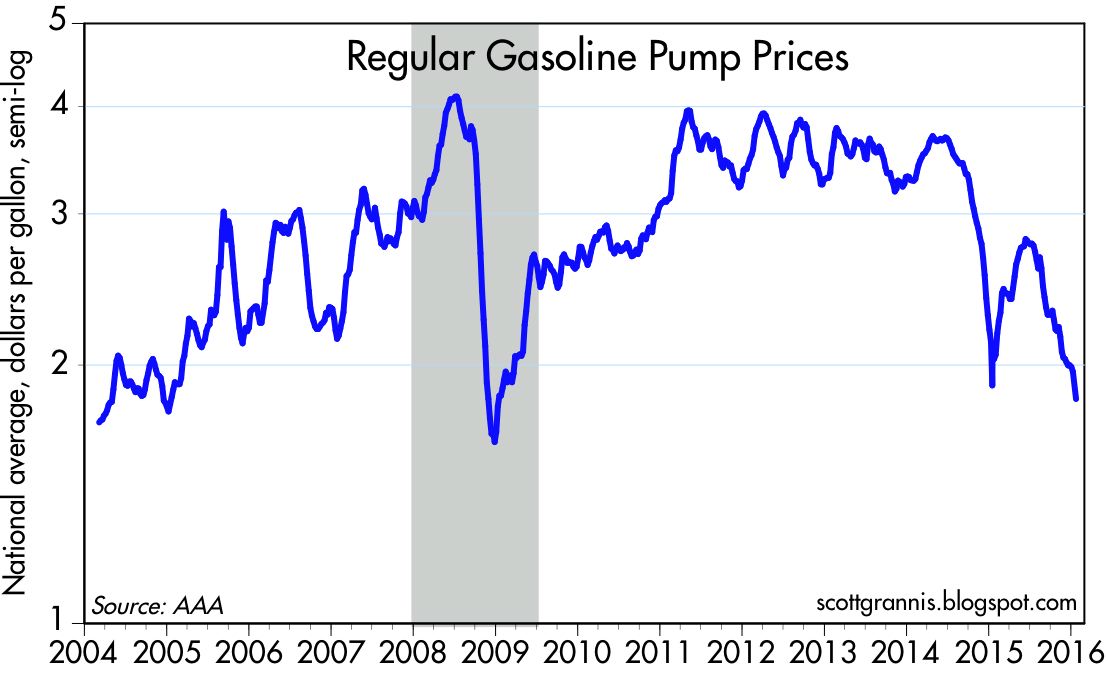

Gasoline prices haven't been this low for a long time.

In response to substantially cheaper gas prices, vehicle miles driven have risen almost 5% since oil prices started to fall in mid-2014. Consumers and businesses are definitely responding to cheaper energy prices. Cheaper energy prices are likely working to stimulate more activity throughout the economy that has yet to show up in the statistics.

As the chart above shows, the big drop in real gasoline prices (shown here as a rising red line) has been an important source of rising consumer confidence.

A survey of small businesses shows that hiring plans continue to improve.

The U.S. consumer is far from being tapped out. Indeed, credit card debt as a percent of disposable income (the red line in the chart above) hasn't been this low for decades. After years of deleveraging, consumers are just beginning to return to the credit well.

This index of industrial commodity prices (CRB Raw Industrials) is up over 4% in the past two months. This leaves commodity prices more than 90% above their lows of late 2001, and suggests that demand is starting to pick up and/or supplies are starting to tighten. Despite the global weakness sparked by the slowdown in China, prices are not going down a black hole.

Bank lending to small and medium-sized businesses has been rising at double-digit rates for over five years. This reflects increased confidence on the part of businesses and banks.

After five years of very slow growth (2008-2013), bank credit is expanding at a more normal pace, up over 8% per year for the past two years.

Confidence is rising, there is no shortage of money or credit, businesses are hiring, cheaper energy prices are stimulating more activity, and the housing market is firing on all cylinders. This is not what you would expect to see if the economy were teetering on the brink of another recession.

18 comments:

And yet home builder's stocks are collapsing. Who is right?

The Bloomberg index of home builders is down about 20% in the past few months, but I note that it fell even more in mid-2013. Not every stock market selloff is a predictor of recession.

Solid post.

Why am I worried? Partly I got the wrong gene pool.

And the Fed. They have consistently overestimated economic growth and inflation, and made their monetary policy accordingly. A monetary noose on the economy is not a pleasing prospect. The Fed has vowed to cinch up four times this year.

Tight? The US dollar is up 25% from recent lows, and is far higher now against a mixed basket of currencies than in 2008.

"Not tight enough," says the Fed.

Scott,

Great information. Read a couple of recent reports that tried to explain current market disconnect.

1) Bill Miller http://www.lmminvestments.com/a-silver-lining-in-the-dark-cloud-of-volatility/ 70% of trading is price action based and not on fundamentals.

2) Riverfront and some others are suggesting the downturn is related to the forced asset sales by Sovereign Wealth Funds due to the drop in oil prices

I see how these things could impact the largest and most liquid names but I'm having trouble understanding how this would impact the stock prices of less liquid names, homebuilders, regional banks etc.

Thanks

Thanks

so dull and repetitive, and (not surprising) misleading on the commodities point.

Many Other Views

So shall we be contrarian to these views? Bet against them?

http://www.barrons.com/articles/byron-wien-heres-why-im-not-optimistic-for-2016-1453839096?

http://www.bloomberg.com/news/articles/2016-01-22/birinyi-more-worried-about-markets-now-than-any-time-since-2009

http://www.bloomberg.com/news/articles/2016-01-21/george-soros-says-he-expects-hard-landing-for-chinese-economy

http://www.bloomberg.com/news/articles/2016-01-12/gundlach-says-stocks-to-struggle-early-before-buying-opportunity

http://www.barrons.com/articles/barrons-2015-roundtable-part-1-a-world-of-opportunities-1452927095

http://www.cnbc.com/2016/01/26/mohamed-el-erian-warns-about-a-day-of-reckoning.html

http://valuewalkposts.tumblr.com/post/136400009155/paul-singer-says-this-is-the-next-big-short

William: the drumbeat of negative news and commentary is intense these days, and that awakens my contrarian instincts.

Scott, mine too.

To open the Barron's Roundtable article, copy and paste the title into Google Search:

Barron’s 2016 Roundtable, Part 1: A World of Opportunities

As many know, this method will unlock many blocked, subscription only articles.

I really appreciate these types of posts. Thank you.

Bankruptcies

There are Bankruptcies coming among oil and commodities companies and most probably bond defaults among developing nations. Goldman Sacks suggested that up to 200 small oil companies related to fracking are vulnerable.

"Last night Moody’s downgraded Freeport McMoRan’s debt from Baa3 (investment grade) to B1 (junk status) reflecting uncertainty about the company’s ability to sell assets within this “fundamental shift in the operating environment”. This was a four notch downgrade which is an unprecedented move outside of a fraud situation."

Freeport’s CDS spread is hitting record highs. Take a look at the CDS chart in the link below;

http://www.otterwoodcapital.com/2016/01/28/commodity-producers-reaching-breaking-point/

29 trillion in corporate debt. No, that number is not wong.

And new home starts are still 1/2 of it's all time high,

with record low interest rates, thanks to the FRB.

Look at the FRB balance sheet and the rise in the stock

market, they are like a couple holding hands, fully embraced,

lips locked and loaded.

This "recovery" is so sick, it should be on Barrocko Care.

Ben Jamin, you are right, the Fed has gone full blown Nipponese.

Five serious and ugly charts! How about that vote of

confidence from the Central bank, by deferring a petty

25 basis points.

The Captain and the crew, whom have been steering the

USA SHECONOMY, for some seven years, now have lost their

collective, nefarious nerves.

We would have been better served, if Chef Ramsey ran the Fed.

https://app.hedgeye.com/insights/48816-from-denial-to-acceptance-the-fed-s-economic-views-cycles-through-the

Thank you, Mr. Grannis. Homebuilders are anticipating credit tightening will spill over mortgage credit. But perhaps investors are jumping the gun and this is the greatest buying oppo since 09', in a much longer run. Only time will tell.

Clinton condo: if you are right, then the market is wrong. We are years away from a tightening of credit. I see no evidence of a scarcity of money or a paucity of lending.

From CNBC:

“The Bank of Japan adopted negative interest rates for the first time at the end of its two-day policy review on Friday, buckling under pressure to ease concerns about the health of the world's third-largest economy.

[T]he BOJ said it will apply a rate of negative 0.1% to excess reserves that financial institutional place at the bank and introduce a three-tier system on rates.

The news saw the benchmark Nikkei shoot up 3 percent, the yen slide 2 percent against the greenback and U.S. stock futures rally 1%.”

--30--

This is a remarkable policy on the part of the BoJ. In contrast, the Fed recently raised IOER to 0.50%.

I am in the camp that does not think these relatively small interest rate adjustments will propel or hinder much lending. Other people, such as George Selgin, say they are important.

I think commercial banks lend when they think they will get paid back with interest, and that means they think there is good aggregate demand. Sure, on the margins, cutting or raising interest rates will do something.

That said, the Fed seems to be moving in the wrong direction. The globe is glutted with manufactured goods, commodities, excess shipping capacity, excess labor, excess capital. Institutional buyers of government debt are projecting 1% US inflation on the PCE for five to 10 years. The Fed uses the PCE, and 2% is an average target. Some target.

It's a joke, as I have never heard anyone at the Fed say, "You know, 3% inflation would be okay for a few years, as we have been under 2% for so long."

The Fed has become ossified, as a federal agency will, and a menace to prosperity and even political stability. It is difficult to suffocate an economy and people into liking free enterprise.

I wish for the U.S. years of "labor shortages" and prosperity.

The Fed wishes for no such thing.

http://stockcharts.com/h-sc/ui?s=%24CRB&p=M&b=1&g=0&id=p30957593652

Perry: the chart you link to is an "excess return" index for commodity prices that results from investing in commodity futures. That is very different from the CRB Raw Industrials index which I have been referring to, which is an index based strictly on commodity prices.

Post a Comment