November industrial production was far stronger than expected, rising 1.6% (including upward revisions to prior months) from October levels. This is one more in a growing list of indicators (e.g., bank lending, jobs growth, the ISM manufacturing index, corporate profits, and commercial real estate) which suggest the pace of U.S. economic growth is accelerating after 5 years of relatively tepid 2.3% growth. However, despite evidence of a remarkable and rather broad-based improvement in the economic outlook, the Fed is still reassuring us that monetary policy will be accommodative for a long time to come. The Fed may be asleep at the switch, but, fortunately, not the bond market vigilantes.

U.S. industrial production is up a strong 5.2%% in the past year, and over the past six months it has increased at a 5.8% annualized pace. The Eurozone, unfortunately, continues to languish. The huge and growing gap between economic conditions here and in the Eurozone helps explain why the dollar has risen almost 20% vis a vis the Euro since 2011. The dollar's strength says more about the relative strength of the U.S. economy than it does about the Fed's monetary policy. But it does jibe with the market's expectation that the Fed is quite likely to begin raising rates in the foreseeable future, whereas the ECB is being forced to resort to more QE.

Activity in the mining sector has softened in recent months, falling by roughly 1%, no doubt due to the sharp decline in oil prices which has surely all-but-halted new drilling and exploration in the sector. The chart above—which excludes the mining and utility sectors—shows strong gains in manufacturing production, which is up 4.7% in the past year, and up at a 5.5% pace in the past six months. Manufacturing production has finally hit a new all-time high.

The story is the same for business equipment production, shown in the chart above. It's up a very strong 6.5% in the past year. The U.S. economy will do just fine even if the mining sector stops growing.

According to the Fed (caveat: the Fed can only estimate, not actually measure capacity utilization) capacity utilization rates in the industrial sector of the economy have reached a post-recession high. As the chart above shows, capacity utilization rates today are almost as strong as they were before the Great Recession. Notably, the Fed's monetary policy stance (as reflected in the red line, which is the real Fed funds rate) has been very accommodative for a very long time. In past recoveries, the Fed responded much quicker to strength in the industrial sector—by tightening policy—than it has this time. This implies that the Fed is running the risk of being "too easy for too long." That (waiting too long to tighten) was one of the mistakes that contributed to the Great Recession and the rise in inflation which followed. Recall that the Fed held rates at 1% from mid-2003 to mid-2004, then began a slow-and-steady policy of raising rates for the next two years. The CPI rose from less than 2% in early 2004 to a peak of 5.6% in mid-2008 (a typically delayed response to a monetary policy error).

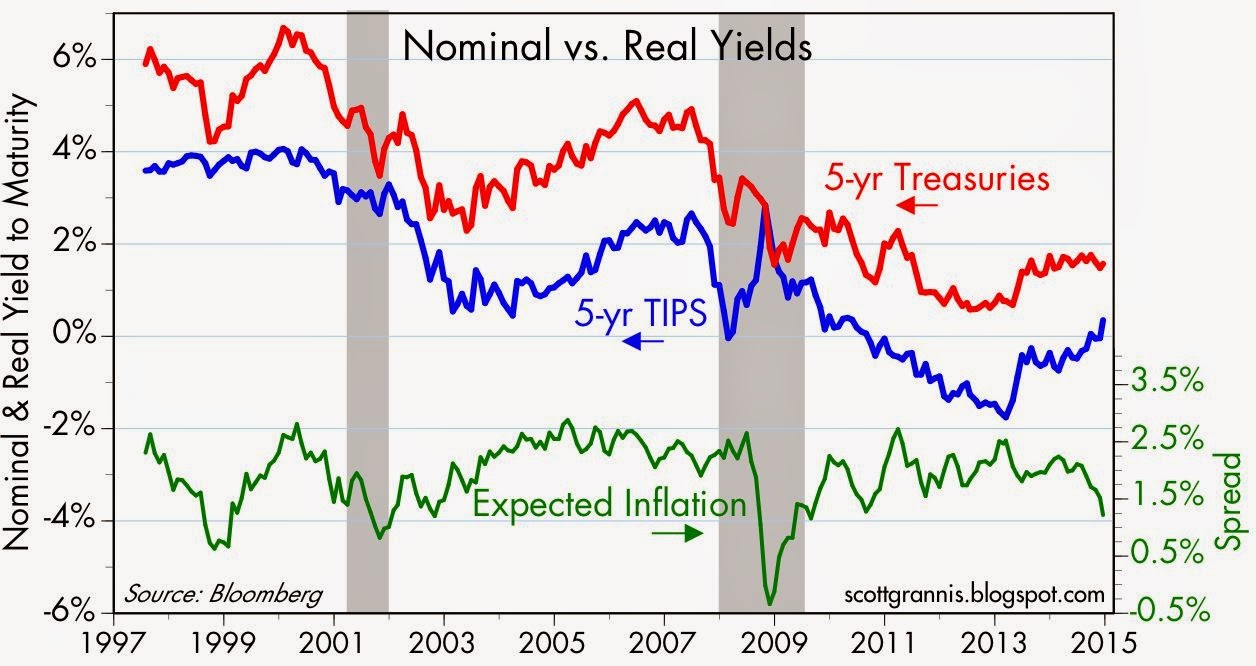

Fortunately, the bond market vigilantes are not asleep at the switch or fearful of the wrath of politicians. Since the end of June, as the chart above shows, real yields on 5-yr TIPS are up 85 bps. The bond market is coming down firmly on the side of an acceleration in economic activity.

The bond market's energetic response to a quickening in the pace of economic activity has gone largely unnoticed, however, because—thanks to plunging oil prices—inflation expectations have declined by almost 1% since June. As the chart above shows, nominal yields have been flat while real yields have risen: last June, the expected rate of inflation embodied in 5-yr TIPS and Treasury prices was 2.14%, and today it is 1.23%. Don't look at nominal yields, look at real yields if you want the "real" story. Real yields are increasing because growth expectations are firming. Nominal yields are not increasing (and in the case of 10-yr Treasury yields, they have fallen by 50 bps since June) because inflation expectations have fallen.

Stronger growth and lower inflation is a terrific combination. But to judge from our skittish equity and corporate bond markets, it's not yet fully appreciated.

17 comments:

Excellent post, Scott.

The Empire State general business headline manufacturing survey dropped 14 points, to a -3.6, the lowest in nearly two years. The bond vigilantes have lots of data to fuss about.

Seems like the only real winners in the US over the past 15 years have been bondholders -- is it the purpose of the US to cater to bondholders at the expense of other investors? I am beginning to believe that the entire world is being ruled by bondholders. Oh well...

Forget about inflation.

The Fed has been tight since Volcker---see long-term trends in inflation and interest rates. If the Fed has been so accommodative, why is inflation headed towards zero?

Scott Grannis has been worried about an acceleration in inflation since 2008, if not 1998.

Well, sooner or later...

The stock market is being driven by leveraged players and they are driven by their interest rate expectations.

Skittish, volatility, and fluctuating, is going to replace melt-up.

Hello Scott,

You post some fantastic, well reasoned and data driven insights. My question - why do you give it all away for free?

Do you just love writing about the topics or want to help people make better decisions?

Whatever the reason is, I am grateful to have come across your site a while back.

Cheers,

Jarrod

yeah, I gotta agree with benjamin on this one. oil's precipitous drop is NOT a universally good thing. when a major tanks like oil has it uncovers a weakness in the system and while it's awesome that opec is getting their asses kicked an unstable russia is worrisome. fed will be at best on hold for awhile and I strongly suspect all these rosy colored economic growth charts won't look so keen a few mos from now.

Scott is an inflation hawk -- he and his allies will worry about inflation no matter what the costs to society -- even war, famine, disease, and death are tolerable by inflation hawks in order to protect themselves from even the worry of inflation -- watch what is happening in Europe -- Dr Draghi is fully prepared to enlist support from the four horsemen of the apocalypse in order to defend Europe against inflation -- that's just the way the world is -- and there's nothing anyone can do to change that reality -- absolutely nothing.

PS: The only escape from the inflation hawks is to join their kind in the top 1% club -- all that is required is to acquire world-class skills that earn premium wages that convert into high-quality dividend and rent-earning equities over a lifetime -- that's the only escape -- everyone else left in the 99% crowd is doomed to a lifetime of misery -- again, the inflation hawks run the world, and the only escape is to join them...

PPS: Here is the reality of capitalism -- my course in life has been to move from the bottom to a higher position in the pyramid -- I commend that approach to everyone...

http://wjmc.blogspot.com/2010/07/capitalist-system-according-to.html

I've only been reading this blog for a year or so. But I think it's an error to characterize Scott as an inflation hawk. I just don't see that.

Scott is a consummate inflation hawk, no doubt about it -- Scott, what's your stand on inflation? More QE or less? Printing more money or less? Staying under the Fed inflation targets, or exceeding? Monetarist or supply-sider?

The ideal rate of inflation? Low and stable.

W McK, Europe's problem is horrible anti-business rules and regulation. Businesses have been commandeered to carry out the socialist manifesto.

WSJ: Foreign Investors Pile Into Bonds

"Foreign investors are snapping up Treasury bonds at the fastest clip in two years, propelling yields to fresh lows even as the U.S. economy gains steam. Purchases by China, Japan, Switzerland and others underscore the broad demand for safe government debt amid global turmoil and uneven economic growth, according to new data from the Federal Reserve and Crédit Agricole.

The overseas buying helps to unravel a mystery that has vexed commentators in 2014: How can bond prices keep rising and yields falling alongside gathering U.S. growth?"

http://www.wsj.com/articles/foreign-investors-pile-into-bonds-1418690550

In fairness to Scott, low and steady inflation is what we have...

Jarrod: Thanks for the kind words.

Why do I do this for free? I posted some relevant comments as to my motives for blogging at the one year anniversary of the blog here:

http://scottgrannis.blogspot.com/2009/09/one-year.html

I do this for free for several reasons. For one, my marginal tax rate on self-employed income is north of 65%, and I refuse to give the government over two-thirds of whatever I might earn by blogging. I'd rather work for free. I also think it's nice to "give back." And by not charging or otherwise benefiting monetarily from the blog, I think that lends it some credibility. I don't have an axe to grind, and I'm not beholden to anyone for anything.

Having said all that, I've long believed that it makes no sense for an economist or a forecaster to charge for his/her services. If your advice is really good, then it's possible to make a lot more money investing your own money than by charging for services to others. Blogging has really helped me focus on my investments and the markets, and that has been very rewarding.

Post a Comment