I didn't think they would do it (QE3), but they did. It wasn't necessary, but I presume that the FOMC was under tremendous political pressure to "do something!" So the Fed will be buying $40 billion of MBS per month for the foreseeable future, and they will also continue "Operation Twist." Their objective is to stimulate the economy, primarily by artificially suppressing mortgage rates, which in turn they hope will stimulate the housing market and thus contribute to a stronger economy. Unfortunately, to judge by key market-based indicators, all they have achieved so far is to stimulate inflation expectations.

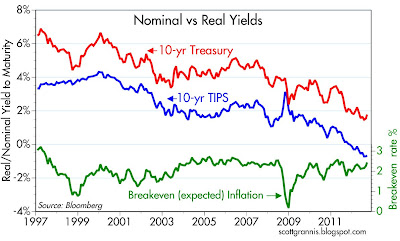

The chart above shows 10-yr Treasury yields (the main reference point for mortgage rates) in orange, and the yield on current coupon Fannie Mae collateral (the benchmark yield for mortgage rates) in white. In the past two months, Treasury yields have risen while mortgage yields have not fallen. The spread has narrowed in favor of mortgage rates, but the level of mortgage yields has not changed. If inflation expectations continue to increase, Treasury yields and mortgage rates will rise.

The Fed can't stimulate without causing Treasury yields to rise, and if they rise further, mortgage rates will have no choice but to rise as well. Rising mortgage rates will be an excellent indicator that the Fed has succeeded in stimulating the housing market. Rates could rise by a lot before they became a burden on the housing market.

The chart above shows the market's forward-looking inflation expectation (i.e., the expected average annual inflation rate over the 5-yr period beginning five years from now). This has now reached 2.85%, up from a low of 2.0% a year ago.

This same result (higher inflation expectations) can be observed in the spread between 10-yr TIPS and 10-yr Treasuries. The average annual expected rate of inflation over the next 10 years is now 2.48%. Not unusually high, but it's clear that the market is figuring that QE3 increases the odds of higher inflation in the future. Not dangerously higher inflation, but the risks of deflation have now almost vanished, and that is presumably a good thing.

The gold market is also treating the Fed's move as a signal for higher inflation.

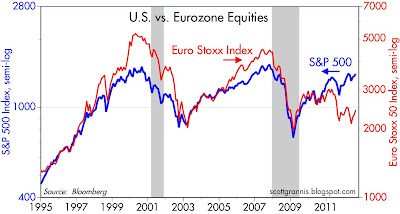

How about the stock market—is it discounting stronger growth, or higher inflation? That's a tough question to answer, but my reading of the market tea leaves suggests that the stock market views QE3 as a sign of stronger nominal growth: businesses are more likely to see improvement in their cash flows in coming years. Whether than improvement comes from more inflation or more growth or both, matters little at this point. Stronger nominal growth means less likelihood of defaults, better profits on average (at least in nominal terms), and less risk of a recession or depression. On balance, the odds have shifted in favor of those who have a claim on future corporate cash flows, so stocks look more attractive. I don't think the market is yet discounting stronger real growth. Let's get nominal growth up and then we'll worry about how much of that increased nominal growth is real and how much is inflation.

I worry more about the risk that the Fed has made an exit strategy from QE more difficult, and thus I worry more about inflation rising in the years ahead. But so far, those fears are somewhat offset by a reduced risk of recession and/or deflation. It's unfortunate the Fed had to come to this, but it's premature to say it's the end of the world.

Regardless, inflation hedges just became more attractive. Seems to me that the cheapest inflation hedge right now is real estate, while the most expensive asset is Treasuries. So: buying real estate using 30-yr fixed mortgage debt (equivalent to shorting Treasuries) looks like an incredibly attractive proposition. With the banking system set to accumulate even more excess reserves, it seems inevitable that banks will want to increase their lending. At the same time, the demand for inflation hedges like real estate should be picking up, and with it the demand for more lending and thus more monetary expansion. Whether this will be good for the economy or just good for the real estate market and inflation hedges in general is a question that will be answered in the next year or two. For now it looks like inflation hedges are the better bet.