2-yr sovereign yields are a good indicator of the market's perceived risk of near-term default. By this measure, the near-term outlook for the Eurozone has improved rather dramatically this year. Yields for most of the PIIGS are still well above German yields, which means they aren't out of the woods yet. But the risk of default is much less today than it was near the end of last year.

Much of the improvement can be traced to the ECB's provision of abundant liquidity to the Eurozone financial market. The reduction in the cost of obtaining dollar liquidity is also significant, as shown in the second chart above. Swap spreads in the Eurozone are still somewhat elevated, but at current levels they signal that market participants are pretty confident that Eurozone banks do not face an imminent crisis. Swap spreads reflect the market's confidence in the health of the financial system, and they also reflect a significant decline in Eurozone systemic risk. The reduction in swap spreads is the market's way of saying that liquidity is decent, that it is possible to trade, that investors and institutions can reduce or increase their risk exposure without much difficulty.

When markets are liquid they can handle almost any problem, because those who are uncomfortable bearing too much risk can shift the risk to someone who is more able and willing to take on the risk. Is there anyone left in the world who is holding onto Spanish sovereign debt that doesn't want to? I doubt it.

5-yr Credit Default Swaps are a good indicator of the long-term perceived risk of default, and here too we see a lot of improvement. Most of the PIIGS now trade better than junk bonds, which means their risk of default is manageable and not very scary.

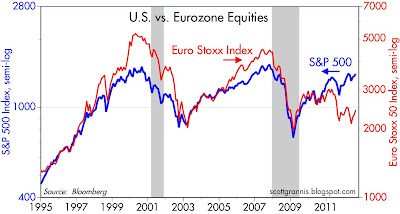

Europe is still struggling, of course, but it's not going down a black hole, which is what markets were very worried about at the end of last year. Even though the reality in Europe is still grim—most countries are probably in a recession, and Spain is having some real problems—things are better than what markets feared, and that is what has put a floor under the Eurozone equity market. The outlook is still bad, but it's not as bad as what had been priced into markets. So on the margin, there has been some noticeable and welcome improvement.

This is the same theme that is playing out in the U.S. The economy still stinks, but we are in far better shape than markets were expecting. Around the end of 2008, markets were priced to something like the end of the world as we know it. Credit spreads were so high than the bond market was effectively expecting that about one-third of the companies in the U.S. would be out of business by now. The market is still very worried about the future, only less so today than before. PE ratios are below average even though corporate profits are at record levels; that tells you that the market fully expects profits to deteriorate. Credit spreads are still somewhat elevated, which also suggests the market expects the outlook to deteriorate. Treasury yields are still extremely low, which tells you that investors are so worried about the risk of investing in anything else that they are willing to forego almost all of the extra yield available elsewhere.

No comments:

Post a Comment