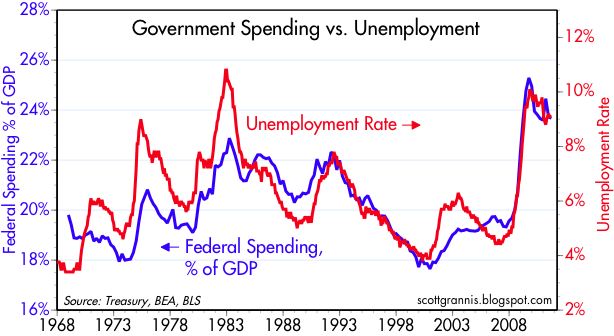

The federal budget numbers for September, released today, didn't show anything encouraging. Revenues came in on the weak side, and the fiscal 2011 deficit was almost exactly $1.3 trillion, second only to the record-setting $1.4 trillion in fiscal '09. Using my estimates for Q3/11 GDP growth, I figure that federal spending is currently running at almost 24% of GDP. If we don't slow the growth in discretionary spending and reform entitlement programs, then the blue line is almost sure to go higher in the future.

What struck me most while updating my numbers and charts was the chart above, which compares spending as a % of GDP to the unemployment rate. There are things like automatic stabilizers (e.g., unemployment insurance) that push spending up when the economy weakens, thus automatically boosting spending relative to GDP, but the extremely close correlation between the two lines since 2008 begs for a better explanation. With no proof, unfortunately, I'm sorely tempted to say that huge increases in government spending only serve to weaken the economy, and that's why a big increase in the relative size of government correlates so well to an exceptionally high unemployment rate. Corollary: cutting back on the size of government would boost the economy and lower the unemployment rate. If the big boost in spending only weakened the economy, then cutting back on spending should help.

15 comments:

Hoisington has econometric analysis that lines up with Scott Grannis' hypothesis about government spending an unemployment. My recollection is that the studies are grounded in theory of Irving Fisher.

Grannis you truly do a nice public service by posting economic data and your thoughts.

‘Keynes was exceedingly effective in persuading a broad group—economists, policymakers, government officials, and interested citizens—of the two concepts implicit in his letter to Hayek: first, the public interest concept of government; second, the benevolent dictatorship concept that all will be well if only good men are in power. Clearly, Keynes’s agreement with “virtually the whole” of the Road to Serfdom did not extend to the chapter titled “Why the Worst Get on Top.”

Keynes believed that economists (and others) could best contribute to the improvement of society by investigating how to manipulate the levers actually or potentially under control of the political authorities so as to achieve desirable ends, and then persuading benevolent civil servants and elected officials to follow their advice. The role of voters is to elect persons with the right moral values to office and then let them run the country‘.

- Milton Friedman, Richmond Federal Reserve Economic Quarterly, volume 83/2 Spring 1997.

http://www.richmondfed.org/publications/research/economic_quarterly/1997/spring/pdf/friedman.pdf

I agree that fiscal stimulus only works if validated by monetary expansionism---and monetary expansionism alone is more effective, driving up private-sector employment, not public outlays and lard.

Would be nice to hire a Bain & Co or McKinsey to devise a plan for US national defense at 2 percent of GDP. That would whack about 4 percent off federal spending, bring it down to the 20 percent range...en route to 16 percent, I would hope.

Correlation does not mean causation -- said another way, more government spending might lead to more unemployment, but more unemployment could simply lead to more government spending -- again, a relationship between two factors does not imply causation.

Scott,

I don't understand how you can be sanguine about the consumer's progress in reducing the debt side of their balance sheet when that debt, and more, has merely been transferred to the Federal Government in the form of increased national debt and Fed balance sheet. The situation for US citizens collectively has only gotten worse, not better, as no true deleveraging has taken place. The reduction in our aggregate standard of living due to the misallocation of economic resources has only been delayed.

Scott says Federal debt doesn’t create new demand. Demand meaning demand for products and services. I believe that just like I know Federal debt doesn’t create money as long as the money is borrowed and not created by the Federal Reserve Bank and given directly to the U.S. Treasury.

But it might be helpful to explain the word ‘new’. Federal debt doesn’t create new demand because, as Scott says, the money is borrowed out of someone’s bank account who now cannot spend the money. But if the person from whom the borrowing came wasn’t going to spend the money, at least for awhile, there is demand that wasn’t there before. It isn’t new demand. It is future demand brought into the present. The problem with federal (and household) debt is that when you get to the future, the demand isn’t there because it already happened in the past. So to replace the demand that already happened now that you are in the future, the Federal debt has to be increased again to bring more future demand into the now present. Eventually you end up at the end of this debt cycle just like Greece where the Federal government can’t borrow and therefore can no longer bring future demand back into the present.

So I will argue there must be an economic contraction in order to adjust to present demand which isn’t amplified by bringing future demand to the present.

That is a good thing. Agreed, Greece should default on their debt and they can start the debt cycle all over again. It makes me laugh. The only way to avoid this is use the proceeds of Federal debt for investment. That is, there is a rate of return on the expenditure of the proceeds. Now that the U.S. is well advanced on this debt cycle, it would be nice to think that we can slowly adjusted to present actual demand based on the structure and conditions of our economy. If we can get growing again, it will go a long way to increase present demand as future demand fades away from the present. It is beyond my wildest dreams that the economy can grow fast enough to actually offset the adjustment processes.

But I long equities since last week as the economy and market often are operating on different time frames.

What do you think about Herman Cains 9-9-9 plan? Laffer seems to like it>

All the basic assumptions underlying Cain's plan are perfect from a supply-sider perspective. Get rid of as many deductions as possible, thus broadening the tax base; tax everyone at a low, flat rate, thus minimizing the distortions that result from graduated rates and high marginal tax rates; and minimize the tax on business, since consumers are really the only ones who pay taxes.

I think the plan could produce spectacular results.

I am uncomfortable, however, with the national sales tax that applies only to new goods. The key objections: it's a doorway to higher taxes down the road; it is potentially regressive; it is a big number to slap on top of state taxes that are also at that level. But consumption taxes do have their merits (very broad base, encourages saving and investment), so who knows how this might come out in the end.

Scott,

Prof. Steve Keen writes extensively about debt, like a negative factor.

Here is his lecture on Australia housing market bubble.

http://www.debtdeflation.com/blogs/2011/03/20/mortgage-finance-association-of-australia-talk/

As his work is very well theoretically founded and only a specialist (like you Scott) can really understand the fundaments of the theory so my humble request to you

Scott, could you please take a look on his view and give us your opinion on that. Thanks very much for your effort, anyway.

Correlation is not causation, as you well know. This is why economics is a branch of political philosophy, not a science.

qwe: Prof. Keen makes the error of asserting early in his presentation that new debt creates new demand, which it does not. And he never explains how it does.

It's amazing how he glosses over this crucial point.

Re Keen. He does trry to explain that Total Spenidng = GDP plus change in debt. Althouhg later in the blog he does concede that some of the change in debt will be reflected in GDP but a significant proportion wont be. Thus he posits that when the essential deleveraging occurs there will be a significant decline in economic activity. Has some good charts.

PS re Keen - he goets quite a lot of exposure in Aus, his work builds on Minsky's - here is a Wikipedia reference

Minsky's theories have enjoyed some popularity, but have had little influence in mainstream economics or in central bank policy.

Minsky stated his theories verbally, and did not build mathematical models based on them. Consequently, his theories have not been incorporated into mainstream economic models, which do not include private debt as a factor. The post-Keynesian economist Steve Keen has recently developed models of endogenous economic crises based on Minsky's theories, but they are currently at the research stage and do not enjoy widespread use.[8]

Minsky's theories, which emphasize the macroeconomic dangers of speculative bubbles in asset prices, have also not been incorporated into central bank policy. However, in the wake of the financial crisis of 2007–2010 there has been increased interest in policy implications of his theories, with some central bankers advocating that central bank policy include a Minsky factor

Of course new debt creates new demand. That is well established in Econ 101 courses even at Chicago and George Mason U.

When the economy is growing normally (consistent with population and productivity growth)the growth is mostly financed with new borrowings (debt) from the banking system.

Post a Comment