This chart shows the market's expectations for where 3-month Libor will be trading in September 2010. By subtracting 30 bps you get the approximate level of the market's expectations for the Fed funds rate over time; currently the market is expecting the funds rate to be about 1.0% a year from now. What strikes me about this chart is that short-term interest rate expectations have dropped since the end of last year—the yield on the Sep '10 contract has declined from 1.9% then to 1.3% today—despite all the obvious signs of an economic recovery that have since emerged. This is one more example of the dichotomy that I mentioned in my

post last Tuesday. Some things—like T-bond yields and short-term interest rate expectations—seem to be priced to a very dismal economic outlook and/or low inflation, while other things—like copper prices, gold prices, a weaker dollar, and swap spreads—reflect strength and a portent of rising inflation.

What follows is my attempt to explain how this all fits together.

At the end of last year the mood of the market was extremely pessimistic, fearing a combination of depression and deflation that would be more terrible than what happened in the 1930s. Since then, the Fed has taken extremely aggressive steps to eliminate the threat of deflation, with the result that monetary policy is now far easier than anyone could have imagined late last year. In addition, the Fed has taken pains to assure the market that policy will remain accommodative for a long time. Fed governors feel comfortable in projecting an extended period of low short-term interest rates given the degree to which the economy is operating below its capacity; this is the Phillips Curve thinking that I've referred to time and again, which can be summarized like this: as long as the economy has lots of idle capacity, then monetary policy

needs to remain very accommodative in order to counteract the risk of deflation. Put another way, with a near-10% unemployment rate, the last thing we need to worry about is inflation. (Note: this is not my view, rather what I think is driving the market and the Fed's view of the current situation.)

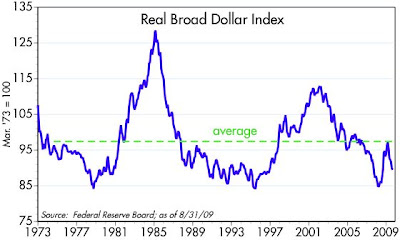

Looking back to the end of last year from today's vantage point, we see that on the margin, there has been a huge change in the market's perception of monetary policy. The market has shifted from expecting monetary policy to be so tight as to generate a prolonged bout of deflation, to now expecting policy to be easy enough to allow inflation of 2 – 2.5%. Such a dramatic easing of policy goes a long way to explaining why the dollar is weaker today than it was at year-end, and why gold is stronger: the supply of dollars has increased relative to what the market expected, and so the value of the dollar has dropped. It also helps explain why 10-year Treasury yields are up 135 bps over the same period, and TIPS breakeven inflation rates are up 160 bps.

But why are 10-year Treasury yields still so low from an historical perspective? (They were only lower on a sustained basis during the Depression.) Why isn't the Treasury market pricing in a higher rate of inflation, given the Fed's massive easing of monetary policy? Why is the market still so apparently eager to buy Treasuries, knowing full well that deficits will be on the order of a trillion dollars or so for as far as the eye can see?

A good friend of mine,

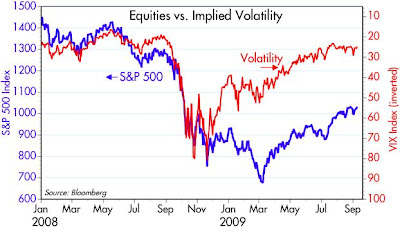

David Malpass, suggests that the dichotomy (relatively low Treasury yields versus rising equity and commodity prices) reflects a market that is investing for two extremes (a "barbell" trade), trying to protect against inflation and deflation at the same time. Buy Treasuries to protect against deflation, since deflation would mean lower yields, while buying equities and commodities to protect against rising inflation. I'm not sure this is a robust explanation (TIPS spreads should be quite narrow, for example, if deflation fears were motivating Treasury purchases), but it does have some appeal and it squares with the continued relatively high level of implied volatility in both stocks and bonds, because it reflects a great deal of uncertainty about the future.

I think we have to look at the mechanics of the bond market for an answer to these questions, and to the pervasive and strongly-held belief that the U.S. economy will be very weak for a long time.

No matter how hard you look, you can't find any evidence today that the bond market thinks the Fed is going to make an inflationary mistake, or that there is any risk of deflation. The breakeven spread on 10-year TIPS is a benign 1.8%; and the 5-year, 5-year forward inflation rate implied by the TIPS market is about 2.25%. As far as the bond market is concerned, the Fed has addressed the deflationary concerns of late last year without jeopardizing the long-term outlook for inflation.

Furthermore, the market apparently agrees with the Fed that there is no need to raise short-term rates for quite some time, since it will be years before the unemployment rate comes back to levels even approaching full employment (variously estimated to be about 5 or 6%). According to the pricing of fed funds and eurodollar futures, the funds rate is expected to be unchanged for another six months or so, and then to creep up only gradually. 2-year Treasury yields today tell us that the market expects the funds rate to average only 0.9% over the next two years. That means you can finance 10-year Treasuries yielding 3.4% for two years and only pay 0.9%, earning a spread of 2.5% per year on average. That's a compelling investment for the bond market, since the Fed is essentially promising that it won't upset the carry trade applecart by raising rates prematurely; the Fed

wants people to borrow and buy things.

As the next two charts show, the slope of the yield curve from 2 to 10 years (which is a good proxy for the appeal of the carry trade) is about as steep now as it has ever been. The steep curve makes for a compelling carry trade. 10-year yields are being held down because 2-year yields are very low.

T-bond yields are thus unlikely to rise unless and until the market realizes that the Fed needs to raise short-term rates sooner than currently expected. When that happens is anyone's guess, of course, but I think it is likely to happen sooner rather than later. That better be the case, however, since being short bonds in a steep yield curve environment has a big negative carry cost. Indeed, it costs over 3% per annum to be short the 10-year Treasury right now. Unless you have a strong conviction that the Fed is going to have to surprise people by raising rates sooner than expected, you would be very reluctant to short Treasuries right now. The Fed, in short, holds the key to why T-bond yields are so low today.

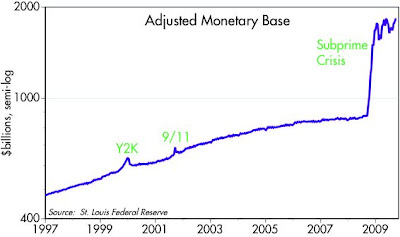

I've been pointing out since late last year that forward-looking, market-based indicators of inflation have all been flashing warning signs: rising gold prices, a weaker dollar, rising commodity prices, a steep yield curve, and rising breakeven spreads on TIPS are all signs that inflation risk is picking up, not to mention the extra $1 trillion of bank reserves the Fed has dumped into the banking system. The market has been studiously ignoring these harbingers of rising inflation because the economy has fallen so far below its potential. Yet these same signs are telling us that the Fed's generously low level of interest rates is progressively weakening the demand for money; people are increasingly willing to borrow (and less likely to hold onto existing money balances) and increasingly willing to buy things like other currencies, gold, and commodities. Which is another way of saying that the Fed is oversupplying money to the system, and this will very likely fuel a higher rate of inflation in the future.

The tension that this creates—the market's confidence in a low inflation future versus the warning signs of rising inflationary pressures—can be found, I submit, in the continued, relatively high level of implied volatility in both the bond and stock markets. And that's how I tie everything together in what I hope is a coherent story.

{kind=link}