As a supply-sider, consumer spending is not one of the things that I pay a lot of attention to. Spending is the by-product of production, so it's better to know whether jobs are increasing or likely to increase, and whether people are working harder and/or more productively, than it is to know how much people are spending. As the late Jude Wanniski used to say, as a nation we can't spend our way to prosperity. It's amazing to me, really, how much attention people and governments pay to spending, as if it were truly the key to prosperity. How can we grow the economy by spending more? Common sense tells you that the economy can only grow by producing more.

Here's an easy example: If I invented a machine which turned the labor of a $10/hour worker into enough food to feed 100 people per day, a lot of things would happen. To begin with, food would get a lot cheaper, and that would allow just about everyone in the world to spend more money on things other than food. A lot of the people employed in the food-production business could devote their energies to other pursuits instead. Some could build me an office. Others could make more food machines. Others could manage all the money I made, by investing it in new startups. And so on. They key to all these changes would be my invention, which allowed one worker to become hugely more productive.

When you consider the world as a closed economic system, it's a mathematical fact that total world spending can only be equal to total income—we can only spend to the degree that we earn, and we can only consume to the degree that we produce. On the margin, changes in spending are not what drive growth, it's changes in income, and income grows only if we produce more. In short: work—and the investment in new stuff which allows people to work more productively—comes first, then spending.

Back to the chart above. What it shows is that the downturn in spending has been much deeper (with the negative growth lasting longer) than in other recessions. But it also shows that the turnaround has been just about as sharp as in other recessions, hence my claim that this is a V-sign. The turnaround has nothing to do with cash-for-clunkers, since that washed out of the numbers by the end of October (i.e., some spending was accelerated, followed by some payback). On balance, real spending increased in 5 out of the six months ending October, and it rose at a 2.6% annualized rate in the four months following the likely end of the recession in June.

This recovery will likely be a little different from past recoveries, however, since the recession was precipitated by a major shock to confidence, and that in turn resulted in a sudden pullback in spending worldwide. So to the extent that confidence returns—and there are lots of signs that it is returning, if for no other reason than that the world didn't end as everyone feared it might—spending could be a leading indicator of improvement. Skeptics argue that fiscal stimulus is responsible for the improvement, but I've been highlighting evidence all year long that confidence was returning and that was a very strong argument for a recovery. We know that money velocity turned up in the third quarter, following steep declines in the prior four quarters; we also know that the demand for money has declined significantly, as reflected in a sharp slowdown in the growth of currency and M2, and in the value of the dollar.

Those are big macro variables that count for a lot more than the meager amount of stimulus that has come from Washington. After all, most of the stimulus is still unspent, and most of what has been spent was in the form of transfer payments that do nothing to stimulate investment or increase people's work effort, and thus do absolutely nothing to grow the size of the economy.

Looking ahead, I see the economy continuing to grow by 3-4% or so. That's not a very robust recovery given the depth of the recession, but it is a lot more than most people are forecasting. Growth is likely to be driven by increases in productivity, something that has been very evident in recent months, and by the natural growth in the number of people entering the workforce. Over long periods, productivity tends to average about 2% a year, while the labor force tends to grow about 1% a year, so add the two together and you get a 3% baseline for growth. But if that's all we get, then it means that the economy is going to have a lot of unused capacity and a lot of unemployment. In a typical recovery, productivity tends to be very strong coming out of the recession, due to strenuous efforts on the part of businesses to cut costs and wring more work out of a smaller workforce. The recovery then strengthens and extends as businesses invest in new plant and equipment and hire more workers.

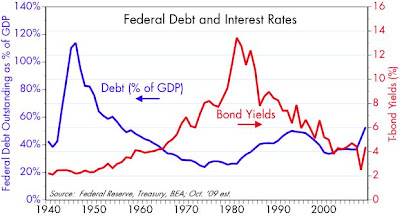

What will keep growth from being robust during this recovery is weak investment. The Obama administration has shown itself to be very hostile to capital, and the prospect of trillion-dollar deficits for as far as the eye can see makes everyone fearful of higher tax rates on work, investment, dividends, and capital. As Art Laffer always says, if you tax something more, you are likely to get less of it. To make the fallacy of Keynesian pump-priming obvious, take the analogy to an extreme: you can't make an economy grow by borrowing money from those that are working and giving it to those who aren't working.

I'm very encouraged when I see that, after a big lurch to the left earlier this year, the political pendulum is now swinging back to the right. The polls have been saying this, and the elections in November confirmed it. There's a lot more work to be done, but my sense is that Congress is going to run out of energy as public support for a "tax and spend without end" agenda continues to wilt. Simply removing the threat of a further increase in spending and regulation could be enough to revive interest in new investments, and that could help the economy in coming years.

Things could be a lot better, to be sure, but there are things to be thankful for this Thanksgiving. One year ago we were standing on the edge of a fearsome abyss, while today we are arguing about how fast the economy is going to grow.

UPDATE: Mark Perry

adds to this meme, noting that "Another V-sign of economic recovery is the turnaround in overtime hours for manufacturing workers. The 23.1% increase over the last seven months, from 2.6 hours in March to 3.2 hours in October, is the largest 7-month percentage increase in manufacturing overtime hours since 1983 following the 1982 recession."