October housing starts came in a bit above expectations, but nothing to write home about. Still, this chart, with its semi-log y-axis, shows that the trend in starts is slightly positive, reinforcing my comments

yesterday about emerging improvement in the housing market. From a low of just around 500K in early 2009, starts now are up over 25%. The level of starts is still abysmally low, of course, but the critically important change on the margin is positive.

Whereas the best that could be said for most of this year was that weekly claims for unemployment were not rising, it's become clear in recent weeks that claims are now declining. We are now entering the time of year when claims normally begin to rise—next month's claims numbers will really tell the tale, since seasonal factors expect a significant rise in claims. But so far it looks like the rise in claims is less than normal, which in turn means that employers have been running a tight ship (having cut staff to the bone) and underlying economic fundamentals are reasonably solid. Since claims are one of the most real-time of all economic indicators, this is very good news.

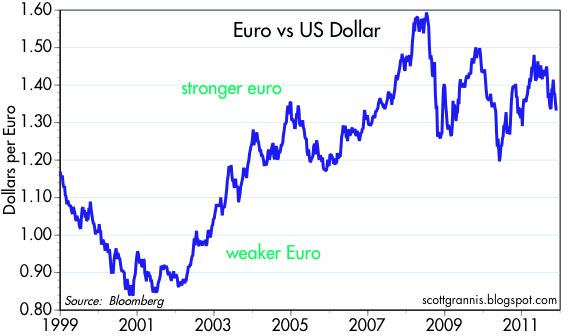

The marginal improvement in both these indicators—echoed in many others such as capital goods orders, industrial production, retail sales, and rising levels of employment—is doubly important given that it is all occurring in the shadow of increasingly dismal news coming from Europe. Imagine how excited markets would be if Europe were also improving instead of teetering on the cusp of a financial meltdown.

So this begs the question: as Eurozone swap spreads approach crisis levels, and as U.S. swap spreads get dragged up to levels that show some emerging stress, are U.S. equities crazy over-priced? Not necessarily. I think it would take a very ugly worst-case scenario to unfold in Europe before the U.S. economic and financial fundamentals would take a hit. Our markets are already very concerned, as reflected in the S&P 500's forward earnings PE ratio of 11.7, in 10-yr Treasury yields of 2%, and in 2-yr swap spreads that have reached 53 today. For things to get nasty, we will need to see some serious defaults in the Eurozone, bad enough to wipe out a good portion of the Eurozone banking system, and bad enough to affect commerce and spark the sort of panic that characterized the economic free-fall we saw here in the latter part of 2008. That could all happen, of course, but it requires some heroic assumptions to be confident that we are on the verge of another catastrophic financial and economic collapse that cannot be prevented. At this point, the absence of more bad news from the Eurozone should count as good news for U.S. markets.

Meanwhile, markets have already priced in a default on Greek debt of monster proportions: 75% (i.e., Greek government debt is priced at about 25 cents on the dollar). That would make an eventual Greek default worse even than Argentina's record-setting default of about 10 years ago. Italian debt is now priced to a 20% default, and that is big news considering the Italian government owes more than $2 trillion. Between Greek and Italian debt, the market has already wiped out about $750 billion.

This loss has already happened. The PIIGS long ago borrowed lots of money and used it to sustain living standards instead of to improve their economic fundamentals. Their economies did not grow enough to service their debt. The market understands this, and has discounted the debt accordingly. Here's what we don't know: is this discount is deep enough or maybe too deep? Who is going to have to write these losses off on their bottom line, and will that cause enough companies and/or banks to collapse to bring down the world economy?

One important thing to keep in mind is that debt represents an agreement to transfer future cash flows. If debt is wiped out, then the cash doesn't get transferred from the debtor to the creditor; the debtor gets to keep it, and the creditor has less than he expected to have. The underlying economic fundamentals—the roads, bridges, buildings, factories, and workers that generate the cash—are not affected. Wiping out debt does not wipe out production or demand. The losses that will eventually be written down have already happened, because the money the PIIGS borrowed was squandered long ago; they never built the added economic capacity to service the debt that lenders expected them to. Bad luck for lenders, but this isn't the end of the world.