Within the past 4-5 months, 10-yr Treasury yields have jumped by 140 bps, and 10-yr TIPS real yields have shot up by almost 190 bps. Most observers attribute this huge repricing in the Treasury bond market to the anticipation of a sooner-than-expected tapering of the Fed's Quantitative Easing bond purchases, and the rise in short-term rates which will inevitably follow. While that's a fair description of what's happened to market psychology,

the more important driver of higher yields is simply the fact that the economic fundamentals have improved considerably.

The above chart shows my interpretation of the intrinsic value of 10-yr TIPS. Real yields that are guaranteed by the U.S. government are a very special animal: nowhere else can you find a fail-safe real return on your money. When real yields were deep in negative territory not too long ago, it was a sign that investors were so worried about the prospects for the economy (and the real profits to be found in alternative investments) that they were willing to forgo any chance of a positive real return. TIPS became extremely expensive because fear was rampant. Now TIPS are approaching what might be considered "fair value" territory. Investors' fears are subsiding, and confidence in the future is returning. This is extremely important because one of the hallmarks of this recovery has been a lack of confidence.

The chart above compares the real yield on 5-yr TIPS to the growth rate of the U.S. economy. Normally, the two ought to bear some resemblance to each other. When the economy was booming in the late 1990s, real yields were 4% because they had to compete with the very strong real returns that investors expected from alternative investments. Today, real yields are returning to levels that suggest the market now believes the economy can grow by 2% a year. That's hardly impressive, but it is a lot better than zero.

We've seen plenty of evidence of a stronger economy in recent months: corporate profits are very near record highs, both in nominal terms and relative to the economy; employment is rising at a fairly steady pace of 190K per month; weekly claims for unemployment have fallen to very low levels; car sales continue to increase at double-digit rates; and conditions in the manufacturing and service sectors have improved, both here and abroad. Federal revenues are up almost 13% in the past year, and they have risen at a 15% annualized pace in the six months ending in July; tax revenues don't rise like this unless there is some real improvement in jobs, incomes, capital gains, and corporate profits.

What's not to like about this? Weekly claims have fallen steadily for four years and are now down to very low levels. Businesses have trimmed just about all the fat they had. Labor market conditions have improved dramatically.

Car sales have been rising at strong double-digit rates for the past four years, and have almost returned to pre-recession levels. This is a picture of a powerful V-shaped recovery. Car sales have exceeded all expectations, and that in turn has caused manufacturers to ramp up production, hiring, and purchases of materials and parts. There are ripple effects from this that have benefited many sectors of the economy already. Housing starts have experienced a similar double-digit recovery in the past two years.

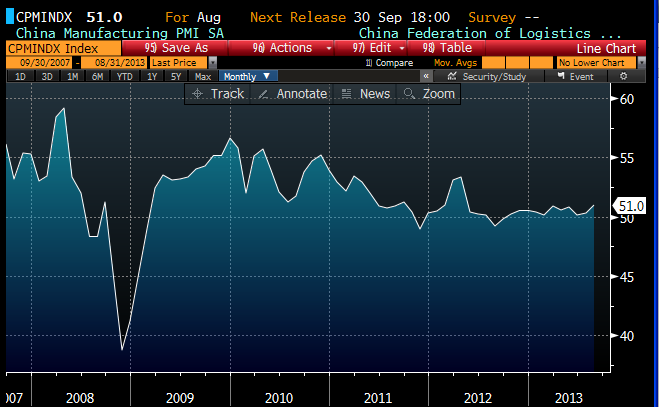

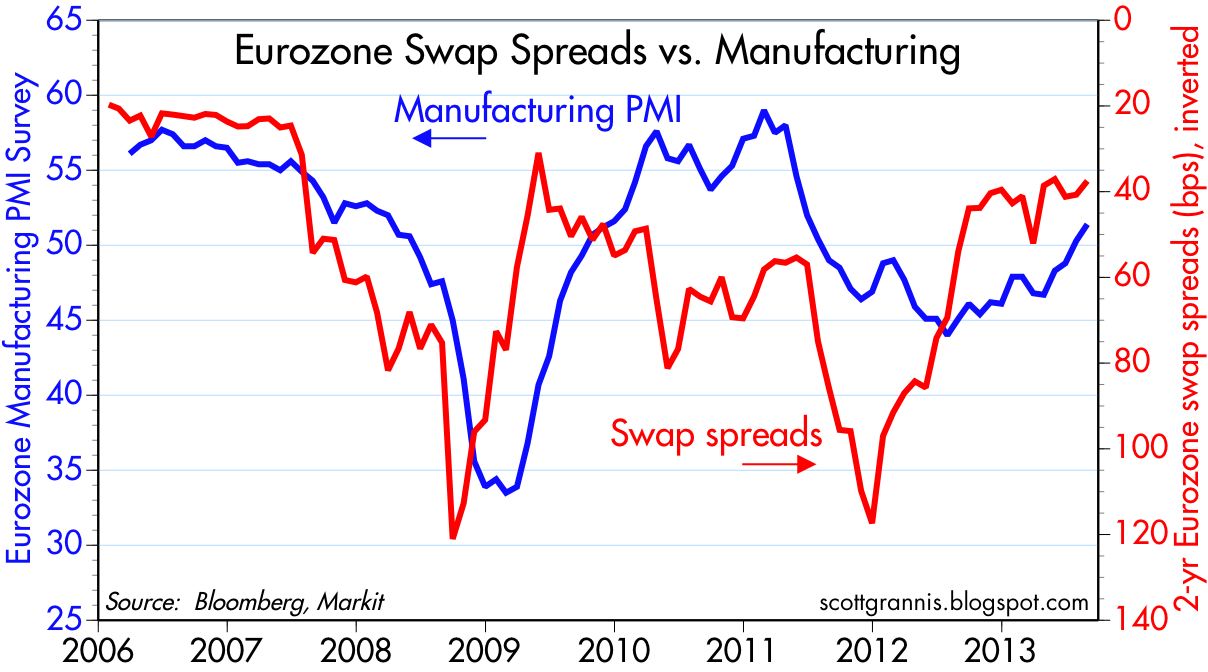

The service sector of the U.S. and Eurozone economies has experienced some surprising strength in recent months. The Eurozone is clearly pulling out of its 2-year recession, and the U.S. economy appears to have regained a surprising amount of strength.

Meanwhile, despite all these signs of improvement, the equity market is still plagued by doubts. The Vix Index rose from 12 to almost 17 recently, while the S&P 500 index dropped 4% from its all-time high. High-yield bonds have shed over 5%, leveraged bond and preferred equity funds are down 15-20%, equity REITS plunged almost 20%, and home builders' stocks gave up 10-25%. Taken at face value, these indicators suggest that the market believes rising interest rates will short-circuit any nascent improvement in the economy and derail the housing recovery that began some two years ago.

This is the sort of "good news is bad news" thinking that is symptomatic of a market that suffers from a shortage of optimism. It's also rather short-sighted, since we know that the economy has been very strong in the past when interest rates were far higher than they are now.

The market's concerns are undoubtedly rooted in long experience with business cycles: e.g., booms are followed by busts, and falling rates are followed by rising rates. But we are still in the very early stages of the current business cycle expansion, and therefore these concerns arguably are premature. After all, it's still the weakest recovery ever, and it will take at least another year or so before the number of jobs exceeds its early 2008 high. And although the Fed seems likely to begin its "tapering" operation soon, the Fed is likely to wait until at least next year before starting to raise short-term interest rates. If the economy should sputter as the market seems to fear, then the Fed could easily postpone any plans to tighten. At this juncture, there is little to fear from the upcoming changes to monetary policy because there is as yet no reason for the Fed to take any dramatic actions; inflation is under control, economic growth is still relatively modest, and the dollar has enjoyed a modicum of support in recent years.

If the market is making a mistake, it's in thinking that low interest rates are stimulative, and high interest rates are depressing; that interest rates are the tail that wags the dog. In reality, however, the economy is the dog that wags the interest rate tail. Low interest rates are symptomatic of a weak economy, and high interest rates go hand in hand with a strong economy, just as low inflation results in low interest rates, while high inflation pushes interest rates higher. I've detailed before why it is that the Fed's

QE is not stimulative; it's primary purpose has been to satisfy the world's demand for safe assets. As the demand for safe assets declines, and as confidence returns, then it is entirely appropriate for the Fed to first taper and then reverse its QE program. The market is now realizing this, and that is why interest rates are up. It's not scary, it's a breath of fresh air.