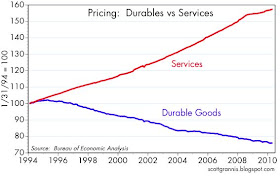

Over the past 16 years the U.S. has experienced a unique condition: the persistence of both inflation and deflation at the same time in two major sectors of the economy. This chart compares the behavior of two of three major subcomponents of the Personal Consumption Deflator: one covers the price of services, which in turn is largely driven by the inflation component of labor costs (and here I note that the PCE deflator rose 40% over the period covered by this chart), and the other covers the price of durable goods (e.g., cars, computers, appliances, TVs, equipment). (The third subcomponent is nondurable goods.) Never before, since the data were first collected in 1959, have these two price indices moved in opposite directions.

What this chart is saying is that consumers' purchasing power, when it comes to manufactured goods, has effectively increased by a lot, mainly because wages have been rising in both real and nominal terms, while the cost of durable goods has been falling. A simple example: for $1000 today you can buy a computer that can do things that not even a computer costing $1 million could do 16 years ago. The widening gap in this chart is a graphical representation of prosperity, where an hour's worth of labor buys more and more things. The difference between these two lines amounts to an increase in consumer purchasing power of a little over 100%, which in turn is solely due to a change in relative prices. The change in relative prices, in turn, is due primarily to the increased productivity of labor. The average worker today (and around the world) is able to produce far more than ever before with a given amount of work. In short, this chart is showing us just how much more valuable labor has become relative to things.

Chinese imports undoubtedly play a key role in this massive and unprecedented divergence of prices. Thanks to the hugely increased productivity of Chinese workers, U.S. consumers can now devote a greater and greater share of their income to things other than durable goods. (Unfortunately, healthcare and government would appear to be absorbing much of this increase.) Currency fluctuations have nothing to do with this, by the way: the dollar has fallen in real terms, relative to a trade-weighted basket of currencies, by about 5% over the period of this chart, so that would have the effect of increasing somewhat the price of imported goods.

The next time you find out that repairing your watch or your computer or your pocket digital camera costs almost as much as buying a new one, remember this chart.