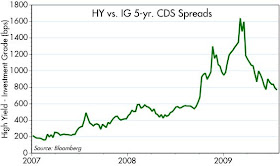

Credit spreads are very important measures of the economy's health, as I've been emphasizing since last October. At that time, a significant decline in swap spreads (a highly liquid proxy for AA bank credit risk—here's a basic primer on what they are) was one of the very first signs that the worst of the credit crisis had passed. The decline in swap spreads has consistently led the decline in other credit spreads, and declining swap spreads have done a pretty good job of foreshadowing improvements in the overall economy. Swap spreads can back down to a semblance of "normal in May, but as these charts show, other credit spreads still have a ways to go. It might take another year for these spreads to come back down to normal. Still, these spreads are making downward progress, and that is essential if the economy is to be on the road to recovery, as it appears it is.

Elevated spreads are a sign that the market is fearful of default risk, and default risk is typically high during recessions for obvious reasons (e.g., money is expensive, cash flow is hard to come by, demand is weak). But with the economy on the mend, money very cheap (banks can get money from the Fed to support lending for almost nothing), and no sign of a general decline in prices, actual defaults are likely to be less than the market is expecting. That in turn implies that high yield bonds and emerging market bonds (where rising commodity prices have dramatically improved the outlook for cash flow) are still attractive investments. High spreads mean relatively high yields, and declining spreads mean rising prices or better price performance relative to Treasuries.

Full disclosure: I am long HYG, EMD, and PAI at the time of this writing.

If you cannot see the boldface lies in Paulson's face I do not know what other proof one can have about a snake oil salesmen before he sells you olive oil as a cure for cancer...

ReplyDeleteHow a former CEO of GS and Treasury Secretary can be stumped like a pimpled faced Freshman in Public Speaking 101 should be enough to give his nation pause.

http://zerohedge.blogspot.com/2009/07/paulson-pwned.html

We are going nowhere as a country fast, but crony capitalism

is alive and well.

Hi,Talking about CDS:

ReplyDelete"European banks including Societe Generale SA and BNP Paribas SA hold almost $200 billion in guarantees sold by New York-based AIG allowing the lenders to reduce the capital required for loss reserves." (Bloomberg). The US tax-payer bailing out European banks?

Besides, there is a growing concern about the future situation of some European banks, due to the massive leverage (I think the ratio in USA in terms of Tier 1 is 1:12 and 1:30in Europe), its current exposure to Eastern Europe and the size of some mega-banks in relation to their countries (such as Credit Suisse and UBS, whose assets go far beyond, several times, the GDP of Switzerland). Do you think this can pose a danger to the prospects of global recovery?

Saludos.

re: AIG - you cannot selectively pay off your creditors*. The government chose to save AIG, and was therefore obliged to pay it's creditors, some of which were European banks. If you object to that either 1) you have to object to the entire AIG bailout or 2) you're in the camp that thinks contract law isn't important.

ReplyDelete* GM and Chrysler excepted.

Antonio: from my macro perspective, the outlook for the banking industry in general and for the global economy has improved dramatically. I can't speak with authority about individual banks, however.

ReplyDeleteHi Scott, thanks for the great blog. Is there a way outside of Bloomberg to watch the CDS index you show above?

ReplyDeleteYou can track these on Markit.com:

ReplyDeletehttp://www.markit.com/en/products/data/indices/credit-and-loan-indices/cdx/cdx.page?#