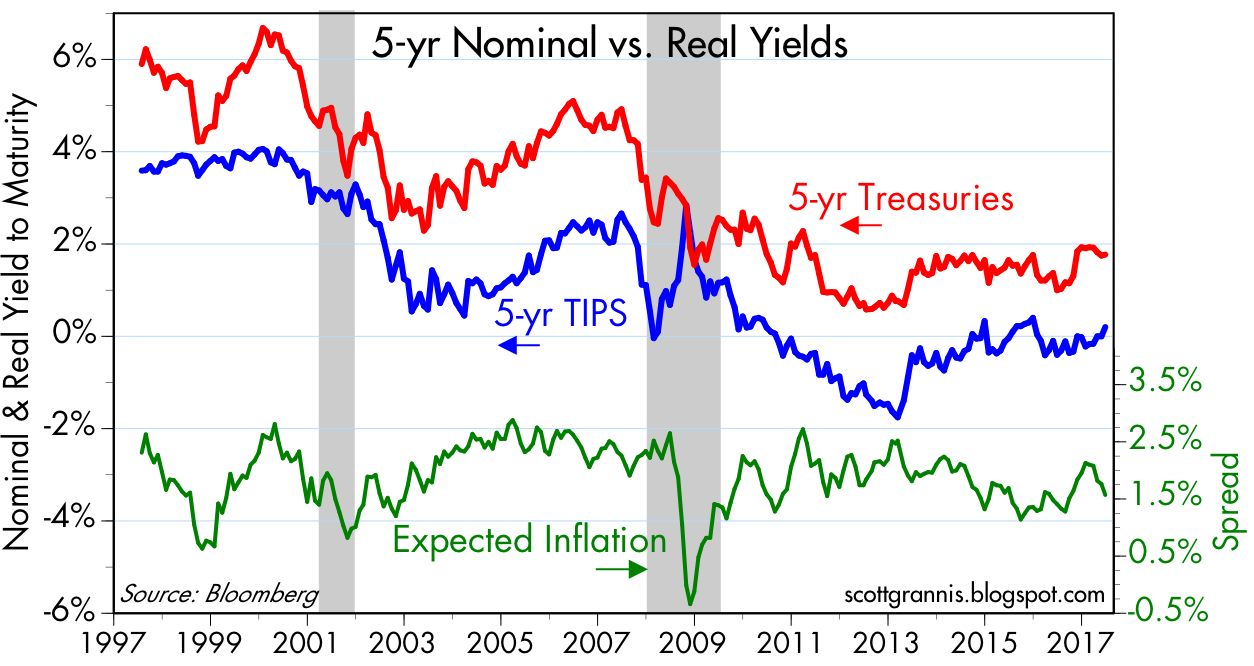

As the chart above shows, TIPS give us direct insight into the market's inflation expectations. Subtracting the real yield on 5-yr TIPS (blue line) from the nominal yield on 5-yr Treasuries tells us the market's implied inflation forecast, which today is 1.6% (i.e., the market expects the CPI to average 1.6% over the next 5 years). Although this is a bit below the Fed's professed target of 2% or so, it is very much within the range of historical experience, and nothing to be concerned about.

As the chart above suggests, the real yield on TIPS also gives us insight into the market's expectations for real economic growth. Real yields on 5-yr TIPS have generally tracked the economy's trend growth rate for the past two decades. Real yields have traded in a narrow and relatively stable range (but with a modest upward trend) for the past four years, and real GDP growth has averaged about 2% over this same period. When real growth averaged over 4% in the late 1990s, real yields on TIPS were just under 4%. That risk free real yields on TIPS should tend to be somewhat less than the real growth of the economy should come as no surprise. The best investors can hope for from the broad market on average is whatever real growth happens to be, whereas TIPS guarantee a real rate of return ex-ante. A bird in the hand should always be worth more (yield less) than two in the bush.

Skeptics might object that TIPS and Treasury prices have been distorted by massive QE-related Fed purchases. But the chart above, which compares the Fed's share of marketable Treasuries to their yield, shows little if any reliable correlation between the two. Today the Fed owns just under 18% of outstanding marketable Treasury debt, and that is about the same share as they held in the pre-2007 period—yet yields today are less than half what they were back then. The Fed currently holds about 9% of outstanding marketable TIPS, so Fed purchases of TIPS have had even less impact on the TIPS market than on the Treasury market.

Not surprisingly, the real yield on TIPS today is heavily influenced by ex-post real yields on Treasuries, as the chart above shows. Fed purchases of TIPS, in other words, are not distorting the real yields on TIPS today. Market-driven real yields are grounded in observable real yields over recent history. And the difference between Treasury and TIPS yields (expected inflation) is very much in line with historical inflation. Again, there is no evidence to suggest that the Fed or the market is distorting the prices or the message of TIPS and Treasuries.

Real yields on 5-yr TIPS are by definition the market's expectation for what the real yield on the Fed's fund rate target will average over the next 5 years. There's an arbitrage that makes this work: you can invest in the Fed funds market for five years or you can buy 5-yr TIPS; in the presence of liquid markets it is reasonable to think that the expected real yield of both strategies is approximately equal.

The Fed makes much of its nominal interest rate target, but it is the real yield on the funds rate that is the most important, and it plays a key role in the Fed's deliberations. Low nominal yields sound like "easy" money, but money is really easy only when real borrowing costs are negative, as has been the case throughout the current business cycle expansion. Real overnight yields are now rising, and beginning to be positive in real terms. That is fully consistent with the Fed's belief that the real equilibrium funds rate is rising as well, since the economy is enjoying improving economic fundamentals (e.g., a low rate of unemployment, steady jobs growth, improving confidence, low implied volatility, low and stable inflation, and reduced regulatory burdens). The current real yield on 5-yr TIPS strongly suggests that the market is expecting the Fed to continue to increase short-term real and nominal rates in coming years, but not by very much. In fact, the market currently expects the Fed to raise its target rate only twice over the next 18 months.

It's also worth noting that the prices of 5-yr TIPS (as proxied in the chart above by using the inverse of their real yield) have been positively correlated with gold prices over the past 10 years or so. This is rather remarkable, given that these two assets are fundamentally different in almost every respect. The one characteristic they share, I would argue, is that both are "safe havens" of a sort. Gold protects against all sorts of risks to one's purchasing power, and TIPS protect against the ravages of inflation of a monetary origin.

Higher real yields on TIPS would therefore be a signal that the market is expecting stronger real growth in coming years. We already see a hint of that in the modest upward trend in TIPS real yields over the past four years, as evidenced in the chart below:

One other thing that we can deduce from this analysis is that there is little if any evidence that the market is overly optimistic about the prospects for US growth. Thus, if Trump and Congress manage to deliver serious tax and regulatory reform, then I would expect to see much higher real yields, much lower gold prices, and a stronger stock market.

As always, great blogging.

ReplyDelete"Low nominal yields sound like "easy" money, but money is really easy only when real borrowing costs are negative, as has been the case throughout the current business cycle expansion."--Scott Grannis

I wonder about this. If the market sets interest rates, then rates are never "easy" or "hard." They just are what they are.

If the world is generating "gluts" of capital, then we should see "low" interest rates, by historical standards. But today's rates may be the new norm, and so only (ahem) older people (including me!) perceive them as "low." Negative real interest rates may become the norm, as the market tries to signal that there is a "glut" of savings.

However, the world has many "forced" savings plans, such as sovereign wealth funds, state pension plans, required insurance (premiums are invested) and large parts of the world where people must save for retirement regardless of current interest rates. Whether savers are free in Red China is whole 'nother question, and they are 1.3 billion people. The world has plenty of capital.

As always, gold is a funny one. Twice in my lifetime gold has utterly failed to keep its value, collapsing from 1980 to 2000, and then again from nearly $1,900 in 2011 to about $1,200 now. A graph of the real value of gold from 1980 to present looks like a roller-coaster trip on LSD and mostly downhill. Yet everyday you see bloggers extolling gold as a preserve of value.

Well, that is the nice thing about macroeconomics and investing, No one is ever wrong and some ideas never die.

James Grant says we soon will hit hyper-inflation, and if not 1985, then 1995, then 2005, then 2015, and you know, the danger lurks constantly, so you should invest accordingly....

OT:

ReplyDeleteI had not realized this, but commodities are down this year by 8.7%, or so say the Bloomberg guys. There are other indices.

https://www.bloomberg.com/quote/BCOM:IND

Bloomberg's commodity index you cite is worthless, overly influenced by oil prices and the pricing of futures contracts. It has been falling for the past six years. I much prefer commodity indices based on market prices and which exclude oil prices (because they are far more volatile than most commodity prices and thus tend to dominated indices that include oil). Look instead to the CRB indices, in particular the Raw Industrials index. It is up 25% in the past 18 months.

ReplyDeletehttps://us.spindices.com/indices/commodities/dow-jones-commodity-index

ReplyDeleteI think all the indices are useful, but probably for different purposes.

The above index is fairly broad, and shows commodities generally falling the last five years, fairly steadily. The all-time peak was back in July 2008.

Been tough to make money in commodities for a long time. There was such a huge run-up in prices pre-2008 that supplies will be lush for a while.

Also, as many people have noted, the long-term price for any physical good, commodity or manufactured, is probably down.

Man is inventive. If markets are free, commodities will get even cheaper.

Benjamin-Gold is up 30% since 2009

ReplyDeleteif you bought SLW in 2009 along with MLP's you are rich right now

they were dirt cheap and paying divis..

GLD was trading at 91.31 on 1/1/09 and is now trading at 118.77 for an acr of 2.8%, slightly more than rate of inflation. Gold is a dumb investment. It's a ROCK! No dividend and no "wind behind the sails" such as incremental growth due to GDP expansion. Never understood it and I contend that most people don't either otherwise would trade much lower.

ReplyDeleteRe commodity indices: There are two types, and they are fundamentally different. 1) indices that are based on the spot prices of commodities, and 2) indices that reflect the results of investing in commodity futures. The CRB indices are the best example of the former, and they show that commodity prices have been rising in the past year or so. The Bloomberg and SPIN indices are examples of the latter, and they show that investing in commodities via futures has been a losing proposition.

ReplyDeleteI always refer to indices that are based on spot commodity prices, because I think they provide insights into the global economy.

Great explanation in commodity indices.

ReplyDeleteWe may see some global growth thanks to the PBoC and the Bank of Japan.

The Fed tightening the monetary noose---the SF Fed recently opined the U.S. is "beyond full employment."

Interesting times,

Steve, you play in paper per your example....Some don't....easily gamed like libor, oil, gold and most other markets now, including the housing market....

ReplyDeletelets be honest, every market has been pushed up by hot money....

so only because of the "Bernanke put" were you able to say other investments were better than gold...

GDP expansion has nothing to do with wind and everything to do with the central bankers 18 trillion and counting across the globe...

I bought SLW at 2 and sold at 38....I have enjoyed that money off that dead investment...

The correct big picture of the US economy

ReplyDeleteis that in May and June bad news economic data releases

have significantly increased.

Data releases include a lot of bad news for April and May

in housing starts, factory orders, durable goods orders, and construction spending

... 2Q 2017 auto sales were down 9% from 4Q 2016

.... industrial production grew only +0.1% in March, boomed +1.1% in April,

and then had no growth in May = puzzling volatility

... over 8,000 stores will close this year, more than any year of the last recession

... US commercial and Industrial loans were growing 7% year-over-year in January,

then declined to only 1.6% y-o-y growth by the end of May -- weakest since 2011

... state and federal government tax receipts are down from 2016

... Automotive News reporter Nick Bunkley tweeted on July 3:

"GM's inventory has officially hit a 10-year high.

980,454 units in stock (a 105-day supply)

as of June 30, the most since June 2007.

After eight years of economic growth,

it is important to look for bad news,

for clues that the next recession is coming,

just as in a recession,

it is important to look for good news,

for clues that the next recovery is coming.

Employment data are not leading indicators.

Employment often goes up in the first month of a recession.

It might be significantly revised a year later,

but real time employment data do not predict recessions.