Those in the market for a fixed-rate mortgage should be sure to study this chart. It's not yet common knowledge that 30-yr fixed conforming mortgage rates hit an all-time low of 3.3% less than 6 months ago, and have since risen to at least 4.2%. It's probably hard to find anything lower than 4.4% today, according to this report (HT Calculated Risk). The days of 3-handle 30-yr mortgage rates are probably a thing of the past.

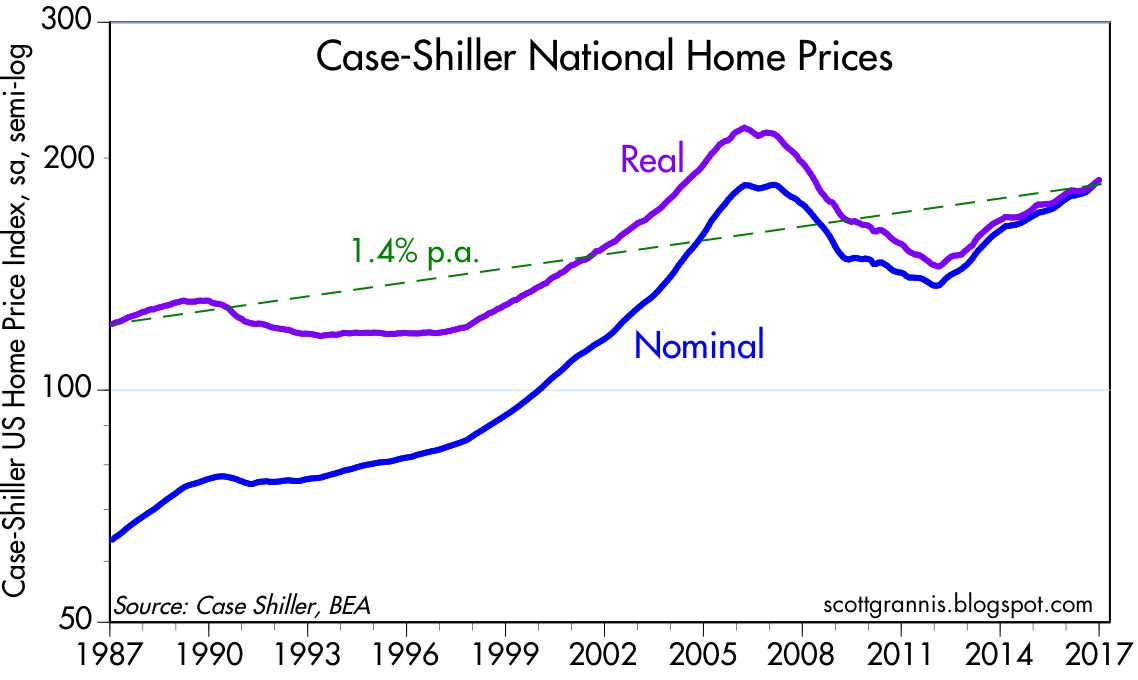

So will rising mortgage rates kill the housing market? According to Case-Shiller, nationwide housing prices have risen at a 6.5% annualized clip for the past 5 years, and have now eclipsed their 2006 highs. In real terms, however, housing prices today are still about 15% lower than they were in 2006, as seen in the chart below:

Higher mortgage rates increase the effective cost of owning a home, so at some point higher rates are likely to slow down the housing market. But for now, I would argue that it's best to think that higher rates are a by-product of a stronger economy and stronger demand. Mortgage rates and housing prices are rising because demand for housing remains strong at a time when lenders are becoming less willing to lend at what are still relatively low rates from an historical perspective. It's all part and parcel of increased confidence and stronger growth fundamentals.

Commercial real estate stopped appreciating back in August. Multi-family apartment sales have slowed way down. I think there is some false life in national single-family detached housing prices, which are often propped up artificially by zoning (verily, we all believe in free enterprise, just not in our own neighborhoods!).

ReplyDeleteToo soon, of course, to say "plateau," "lull" or "top" on property markets.

Given that the PCE YOY is at 1.7%, I wonder why the Fed is raising rates now.

The risk is here: Real estate lending if how a lot of new money enters the economy. About 50% of bank lending is on real estate. It is a misnomer to talk about "commercial banks." They really should be called "property and commercial banks."

If real estate starts drifting down, hard to see much economic expansion ahead.

The Fed appears imprudent and reckless presently, adhering to outdated nostrums. A globalized economy does not appear inflation-prone, but does appear to suffer from a lack of aggregate demand.

Another threat: the banks are sitting on huge reserves. Even an eight-year recovery could not get them to lend the bulk of their reserves out. Now they will be getting more interest from the Fed, through IOER, to sit on their reserves. I think 0.75% at next rate hike. That's a nice bit of risk-less, effortless return.

I hope the Trump enthusiasm and pro-business moves carry the economy through 2017.

The Fed might kneecap Trumponomics, however.

Benjamin: Excellent points, all. One comment: I'm thinking the monetary environment is similar to that of the second half of 2004. Recall that the Fed started a 17-move rate hiking policy in mid-2004 and it would last two years taking the Fed Funds from 1.0% to 5.25%. But in the first year of that move, the real Fed Funds rate was well below the 5-year TIPS spread (as Scott has shown on many occasions with that great chart). My point is that, like then, we're clearly in a rate-hiking cycle. This should raise the yellow flag, for obvious reasons. But on the question of whether or not the Fed is too tight, I'm leaning against that conclusion right now for the reason noted above.

ReplyDeleteBut your comment regarding bank lending on real estate is a very good one. This (so far) paltry lending may take the oomph out of this recovery. We shall see.

Long end rallied and gold miners shot up 7-10% within an hour of the Fed hike. WTF? Sell the rumor, buy the news? Financials didn't want to rally with the curve flattering. Odd to me.

ReplyDeleteFlattening

DeleteThis comment has been removed by the author.

ReplyDeleteScott has been pointing out for quite some time that money demand has been huge compared to historical levels. If so, then one could guess that money is entering all asset markets, but of course to differing amounts depending on ones preferred asset allocation.

ReplyDeleteThis continues to be a fascinating economy to watch. Especially with the unexpected fiscal policy changes. I can't wait to see how this interest rate cycle unfolds.

Also, it looks like volumes on the Dow and S&P are now back to pre-crisis levels. I'm scared of TMC to GDP but Scott's graph differs from Guru focus. The holy grail would be closure of the output gap but every smart person I've watched doesn't think we'll get back to the historical GDP potential of roughly 3 to 3.5%.