Both the services and the manufacturing ISM indices confirmed that activity picked up towards the end of the first quarter, all but erasing the earlier slump. This likely means that the economy is back on the 2% growth track that has prevailed for the duration of the current business cycle expansion.

The employment subindex is once again back above 50, but only reflects modest improvement in employment going forward.

The U.S. and Eurozone economies have been tracking each other for the past 3-4 years, with both growing moderately.

The chart above compares the growth of prices in the service, non-durable, and durable goods sectors. Since 71% of the US workforce is employed in the private service sector, and since the cost of services is largely determined by wages, we can infer that the vast majority of the US workforce has been enjoying very healthy wage gains relative to durable goods prices. Service sector prices have been increasing at a modest 2% annual rate for the past several years, but they have increased two and a half times faster than durable goods prices since 1995 (which happens to mark the start of China's huge export boom).

This is equivalent to saying that an hour's worth of work in the service sector buys 2.5 times as much in the way of durable goods as it did in 1995. We can lament the tepid growth in median incomes over the past few decades, but this significantly understates the gains in workers' purchasing power for durable goods. Practically anyone who works these days is able to afford a smartphone, a device that replaces goods that would have cost a small fortune just 20 years ago. Let's not lose our perspective: things could be a lot better, but they could also be a lot worse.

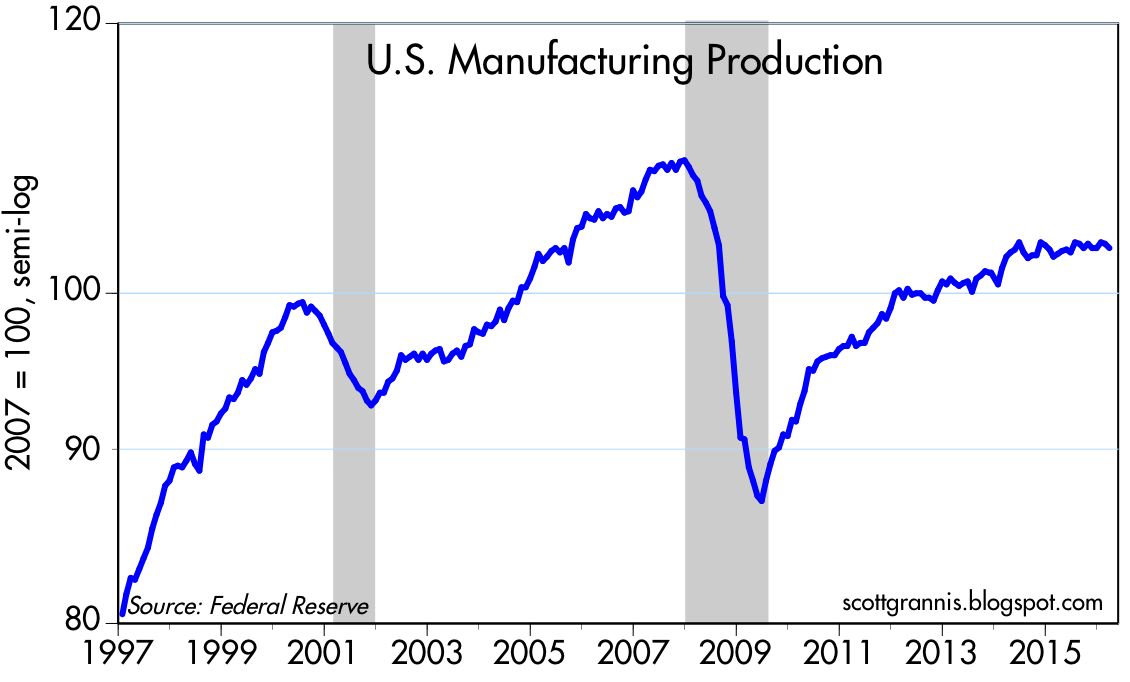

Industrial production and manufacturing in general have been the weakest sectors of the economy in recent years. Industrial production has been declining for almost 18 months now, but the lion's share of that decline can be traced back to the huge reduction in oil-related activities, which in turn are a logical response to plunging oil prices. As the next chart shows, manufacturing production has been flat for the past 18 months. Most of that weakness undoubtedly stems from declining production of energy-related equipment. Outside of the energy industry, life goes on in a relatively normal fashion, but with the under-appreciated boon that cheap energy represents to the vast majority of consumers.

No comments:

Post a Comment