The Bloomberg index of financial conditions is at an all-time high, which suggests that financial markets haven't been this healthy for the past two decades. This index is composed entirely of real-time measures of market sentiment, risk aversion, liquidity, credit risk, and profit expectations. No seasonal adjustment factors were used in the manufacture of this index, and no revisions will ever be made to the data. This index has a good record of leading economic conditions in general, and currently it is saying that there is virtually no risk of any significant economic disruption on the horizon.

Very healthy financial conditions are like a big green light for investors, especially these days, since the yield on cash and cash equivalents is almost zero. Holding zero-yielding cash when the economy is very likely to continue growing is a very expensive undertaking, since it means foregoing the much higher yields available on risky assets, as shown in the chart above. Holding cash only makes sense if you are very worried about the economy stumbling, but financial indicators say that the risk of that happening is extremely low.

By setting the yield on cash at an extremely low level, the Fed is essentially urging investors to take on more risk. It's ironic that the Fed's extraordinarily accommodative policy stance is still interpreted by most observers to be reflective of a deep and abiding concern over the recovery's fragility. Instead, as I've argued repeatedly, the Fed has in effect been forced to adopt an extraordinarily accommodative policy stance because the world has been so very risk averse.

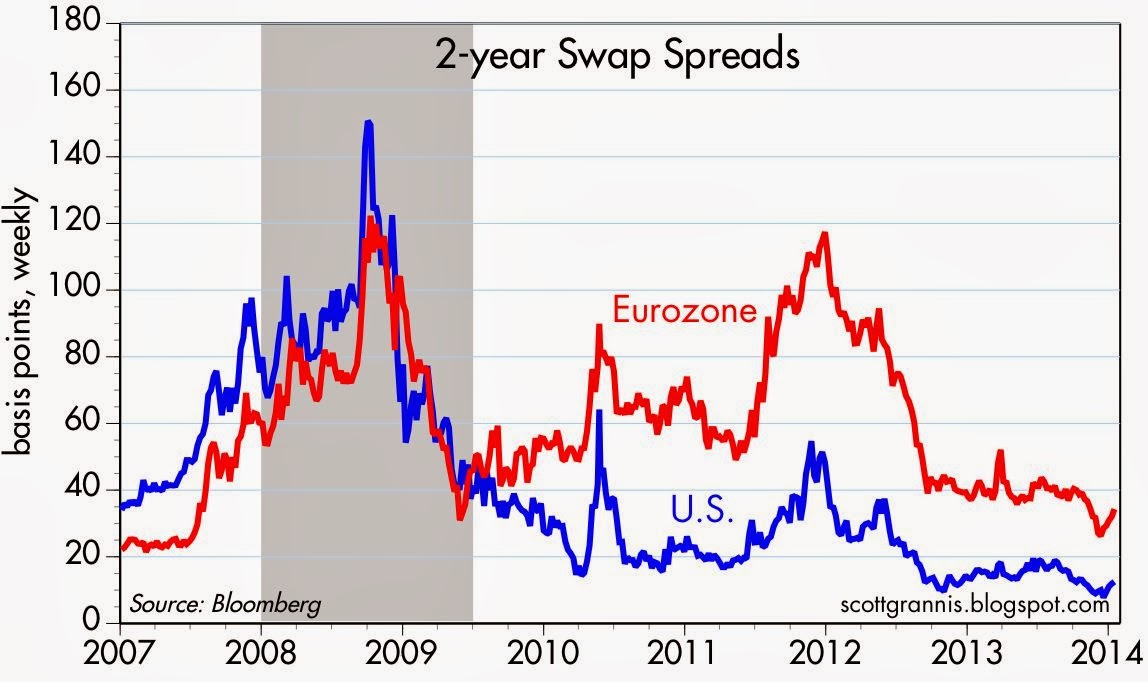

Swap spreads, shown above, are one of the components of Bloomberg's index. They are indeed very low, which is very good. This is a direct reading of the market's liquidity and the systemic risk currently to be found in the markets and the economy. Things just don't get much better. Eurozone conditions aren't quite as attractive or healthy, but they have improved significantly in the past two years.

As the above chart shows, swap spreads have been excellent leading indicators of the economic health of the economy, rising meaningfully in advance of recessions, and falling meaningfully in advance of recoveries. (A short primer on swap spreads can be found here.)

currently it is saying that there is virtually no risk of any significant economic disruption on the horizon....is there a more cringe inducing statement anyone can say? I've got to admit to being fully invested, but also know I'm at my best in times of disruption....

ReplyDeleteI hear you, but these are market-based indicators that have little to do with opinions or sentiment. That's a key distinction. When everyone believes the good times will continue to roll, that is when it pays to be nervous.

ReplyDeleteI note that swap spreads were elevated in 1989, well in advance of the 2001 recession, yet sentiment from 1989 through early 2000 was incredibly bullish. Real yields on TIPS were 4%, implying the market saw 4% real growth or better for as far as the eye could see. Elevated swap spreads were completely at odds with very high real yields.

Today real yields are still very low (reflecting pessimistic growth assumptions), but swap spreads are very low also (reflecting a very healthy growth outlook). So things are at odds again, but this time the other way around.

Regarding Treasuries as of moments ago according to Bloomberg:

ReplyDelete10 Year 2.7500 99-06 2.85% -4 +102 14:27:54

30 Year 3.7500 99-19 3.77% -12 +77 14:44:15

Should treasury rates increase to perhaps 9-10%, I will have to ponder shifts into bonds -- I would be interested in acquiring Treasuries with 9-10% plus interest, especially on 10-year and 30-year Treasuries...

No way I would be in cash right now...

PS: Should treasuries head into 12-14% interest, I will be very eager to acquire bonds -- right now, I like dividend and rent-earning equities...

ReplyDelete