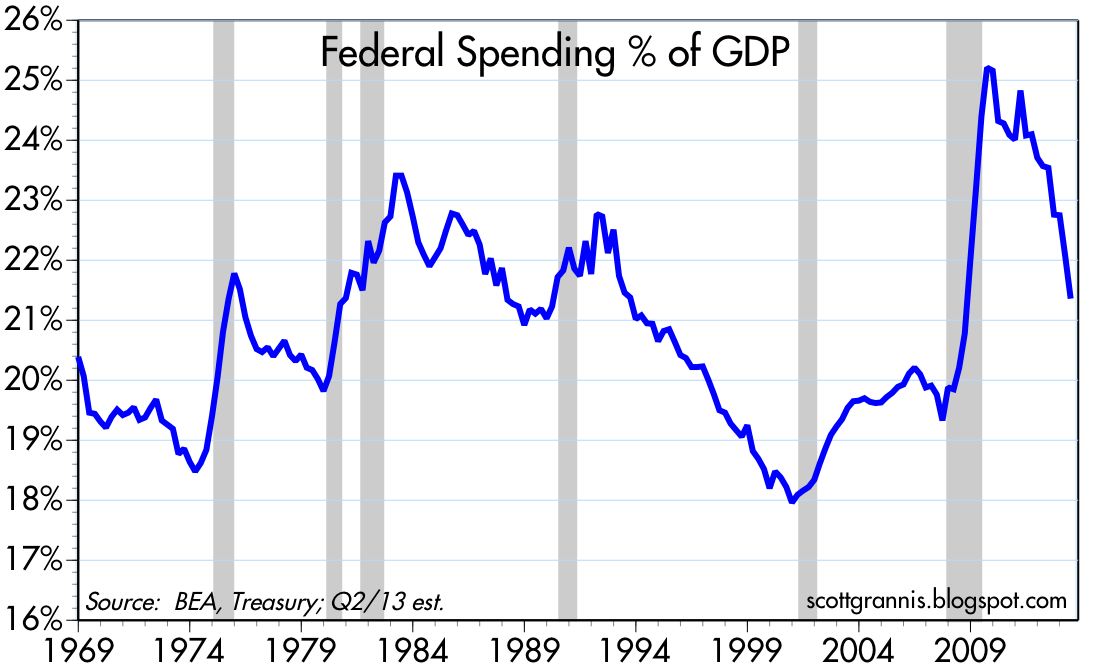

Federal spending fell 6% in the year ending June 2013, by far the biggest one-year decline in the past 43 years. Relative to GDP, spending has declined by almost four percentage points over the past four years, from a peak of 25.2% to 21.4%.

Revenue rose over 13% in the year ending June 2013. Relative to GDP, revenue has increased by a little over 2 percentage points, from a low of 14.6% in 2009 to now 17%.

The deficit has declined from a high of 10.5% of GDP in 2009 to now only 4.4%. In dollar terms, it has fallen by more than half, from a high of $1.48 trillion to just under $0.7 trillion.

A variety of forces are at work behind the scenes of this dramatic improvement. Congress has been deadlocked for several years and unable to agree on new spending legislation. The budget sequester has kept some spending from increasing. The economy has been slowly but steadily improving, generating some 7 million new jobs, an almost $2 trillion increase in personal income, and about a one-third organic increase (i.e., unrelated to higher tax rates) in personal income tax receipts. The number of people receiving unemployment insurance has declined by more than 7 million, thus reducing "safety net" spending. Marginal tax rates have increased on upper income earners, causing many to accelerate income and capital gains realizations. Corporate profits have increased some 65%, and taxes paid by corporations have more than doubled, from a low of $122 billion in 2009 to $272 billion in the past 12 months.

From a Keynesian perspective, it's remarkable how well the economy has done in the past four years given what has amounted to a huge and wholly unexpected increase in fiscal austerity (i.e., a 6 percentage point reduction in the budget deficit relative to GDP). From a supply-side perspective, it's refreshing to see how much can be accomplished by the private sector in the face of serious fiscal headwinds (e.g., big increases in regulatory burdens and rising marginal tax rates): even just 2% GDP growth per year can solve lots of problems if the government gets out of the way.

This is all very encouraging because the huge decline in the deficit—which is now back to levels that are quite manageable—all but eliminates the need for still-higher tax rates. Indeed, it even opens up the possibility of lower tax rates in the future. The bi-partisan tax reform effort now underway, led by Sen. Max Baucus and Rep. Dave Camp, could produce dramatic pro-growth results if done correctly. That would be the best news I could hope for, outside of a permanent delay to Obamacare, which would almost certainly boost federal spending with little or no benefit to the economy.

Terrific wrap up of federal taxes and spending.

ReplyDeleteWorth noting is that despite the strident caterwauling, federal taxes as a share of GDP have been more or less steady, in fact declining a bit, since the 1960s. I wish they were a lot lower, but they are not getting higher.

What has changed is the composition of federal taxes, shifting from income taxes (corporate and personal) to payroll taxes.

That is not the picture painted by many however.

I wonder if either political party ever has a sensible story line....

BTW:

ReplyDeleteStocks soar to new records on hopes for continued stimulus

Los Angeles Times - 49 minutes ago

The stock market streaked to new highs Thursday as investors remained hopeful that the Federal Reserve's easy money policies will continue to drive the U.S.

--30--

Well, you know what they say. If the market agrees with your analysis. cite the market and efficient market theory and how smart everyone is on Wall Street.

If Wall Street disagrees with your analysis, then say the market is reacting to hidden news, or point out the times the market was wrong....

Boy, QE is not working?

We just hit an all-time record high on the Dow, after the worst recession since the Great Depression. The market has doubled since 2008.

Should we credit Obama? Residual effects of the Bush administration?

I say QE is a good idea, and we need more of it.

Evidently, Wall Street agrees with me. But then, as they say, if Wall Street agrees with you, cite Wall Street...and if it doesn't....

Schaeffer's Investors' Intelligence" Sentiment of Investment Advisers

ReplyDeleteDate...Bullish...Bearish

07/10....46.9....22.9

07/03....43.8....20.8

06/26....41.7....25

06/19....46.8....21.9

06/12....43.8....22.9

06/05....45.8....20.8

05/29....52.1....19.8

05/22....55.2....18.8

05/15....54.2....19.8

OECD Composite leading indicators point to diverging growth patterns in major economies

ReplyDeleteComposite leading indicators (CLIs), designed to anticipate turning points in economic activity relative to trend, point to diverging patterns across major economies. The CLIs point to moderate improvements in growth in most major OECD economies but in large emerging economies the CLIs point towards stabilising or slowing momentum.

The CLIs for the United States and Japan continue to point to economic growth firming.

In the Euro Area as a whole, the CLI continues to indicate a gain in growth momentum. In Germany, the CLI points to growth returning to trend. The CLI for Italy continues to point to a positive change in momentum while the CLI for France points to relatively stable momentum.

The CLIs for the United Kingdom, Canada and China point to growth close to trend rates and the CLI for India points to a tentative upward change in momentum.

On the other hand, the CLIs for Russia and Brazil point to slowing momentum. The OECD Development Centre's Asian Business Cycle Indicators (ABCIs) suggest that the ASEAN’s growth momentum remains resilient overall.

Ben Jamin, Qe is working on Broad St or the economy or both?

ReplyDeleteEither Bank Bernank received a telephone call from his pals on Wall St(to stop the slide)or he has reservation about the health of USA Incorporated...

I am an investor in the markets, however, in the past several years we have gone to mainly cash do to Fedrigging of the markets..

Yesterday, was just another example of Bank Bernank works for all to see...

Regarding the total of fed spending vs GNP, the Heritage Foundation said that 2012 fed spending was 23% of GNP.

ReplyDelete"As this 2012 edition of Federal Spending by the Numbers shows, total federal spending for fiscal year 2012[1] reached $3.6 trillion, or 22.9 percent the size of the entire U.S. economy. In the past 20 years, federal outlays have grown 71 percent faster than inflation. The average American household’s share of this spending is $29,691, roughly two-thirds of median household income. This relentless growth is projected to continue, pushing total government outlays to $5.5 trillion a decade from now, and to about 36 percent of gross domestic product (GDP) in the next 25 years."

I have reservation about anything BEA...

Conspiracy Theories are a poor basis for investing, most folks would agree. It is best to deal with facts as Scott Grannis does so superbly.

ReplyDeleteAs an example, consider Hans comments above:

Conspiracy Theories: "Either Bank Bernank received a telephone call from his pals on Wall St (to stop the slide) or he has reservation about the health of USA Incorporated..."

Investment Decision: "in the past several years we have gone to mainly cash do to Fedrigging of the markets.."

Ben Jamin, you can see the slow but steady creep in Federal spending (socialism) since the turn of the century; completely unabated in any decade..

ReplyDeletehttp://www.usgovernmentspending.com/us_20th_century_chart.html

William, if you do not believe that first and foremost that the Central Bank works on behalf of its institutionalize bank members then you are short on your facts.

ReplyDeleteThese club members are also very active traders and investors on Wall Street itself and would benefit greatly on being first informed...

I do believe you understand the impact upon markets from Fed words and actions. There are few entities or events have such massive influence upon capital markets...

Government, having such grave influence upon investments, is in my opinion not only unhealthy, unwise and certainly damaging...

Ask your local passbook saver what the Federal Reserve has done for them !

This comment has been removed by the author.

ReplyDeleteInteresting read from the FRB - St Louis..

ReplyDeletehttp://research.stlouisfed.org/econ/bullard/pdf/Bullard_OMFIF_GoldenSeriesLecture23May2013Final.pdf

"Announcements that policy will be accommodative far into

the future can be interpreted by the private sector as “the

central bank thinks the economy will never recover.”

This is the problem of pessimistic signaling.

In general, any attempt to provide additional policy

accommodation today by promising easy policy in the future

can be viewed as suggesting the future will be characterized

by poor macroeconomic performance.

This can be extremely counter-productive, as firms and

households may prepare for a prolonged stagnation."

Did Uncle Ben violate this common sense argument several days ago, by announcing the continuation of current "accommodating policy."

Hans-

ReplyDeleteI would like less federal spending. Much of the increase in federal outlays is "only" Medicare and Social Security outlays.

In a perfect world, these programs would not exist, but in another sense they just take my money and give it back later.

Much worse: When the federal government places taxes on my income, they take it forever and spend it on a parasitic agency.

I would like very large cuts in federal agency spending.

As for Bernanke, I think the record shows the Fed has been far too timid in spurring growth, and far too fearful of inflation.

Ben Jamin, agree and a good post!

ReplyDeleteWhat I find disturbing is the lack of information on the Fed's website (http://www.federalreserveonline.org/search/index.cfm) about the basic facts of QE...

Yes, William, that is why and how rumors and conjecture begin because in the current Beltway there is absolutely no transparency...

I enjoyed this thread by, Mr Grannis, until the second to the last paragraph which, IMHO, could have been left out...

Mr Bullard, President of the FRB - St Louis, makes it plain that QE has had an affect on the capital markets...

The Dow (DJI) has had only a single correction of 10% or more since 2009 of March, which occurred in August of 2011...This period is now 52 months old...(12,600 to 10,800)

This article indicates, that real federal spending between 08 to 12 is up..

ReplyDeleteWho is right, whom is wong?

http://cnsnews.com/news/article/real-federal-spending-82290-american-2008

William, this is why so many investors are angry with the establishment! I hope you understand.

ReplyDeleteTrader Dan & Rick Santelli, (I deeply admire him) thoughts on the FRB; Uncle Ben; and "Tap out Taper."

Bring the mudders in!

http://traderdannorcini.blogspot.com/2013/07/rick-santelli-echoing-my-sentiments.html