Who says banks aren't lending? Banks are lending by the bushel. Commercial & Industrial Loans are a good proxy for bank lending to small and medium-sized businesses. These types of loans are up 13% over the past year, and have now posted a net increase of over $300 billion in just the past two years.

Money is in plentiful supply. The M2 measure of money is up over 8% in the past year, and has jumped at a 12.8% annualized rate in just the past 3 months. On a nominal basis, the M2 money supply has increased by over $3 trillion in the past 5 years. That works out to $1.6 billion per day.

Most of the increase in M2 has come from bank savings deposits. Despite the fact that they pay almost nothing in interest, the public has added almost $3 trillion to their bank savings accounts in the past four years. That translates into growth of over 10% per year. The huge increase in savings deposits is the flip side of the public's confidence in the future: low confidence and extreme risk aversion have persuaded households to sock away massive amounts of money in bank deposits. This is money that could be turned loose to fuel a significant boom in growth and prices once the public begins to regain its confidence in the future.

Car sales are up at a 13% annualized pace since their recession low. This is now the most incredible recovery in auto sales on record.

U.S. crude oil production is up 40% in the past four years, and up 20% in just the past year, thanks to new fracking technology. And the boom is just getting underway.

These two charts could be the most bullish of all. Natural gas production (top chart) is up by one-third in the past six years. The huge increase in natural gas production has caused the price of natural gas to decline by about two-thirds relative to crude prices (bottom chart). The U.S. now enjoys a huge advantage over other countries because it has easy access to the world's cheapest source of energy (natural gas). The huge change in relative prices is almost certain to cause monumental changes throughout all the industries that are energy intensive, as companies switch from crude to natural gas. This dramatic change in the type of energy we use and its price could have a major impact on U.S. growth in the coming years.

After four years of a devastating collapse, housing starts are now up 58% in just the past two years!

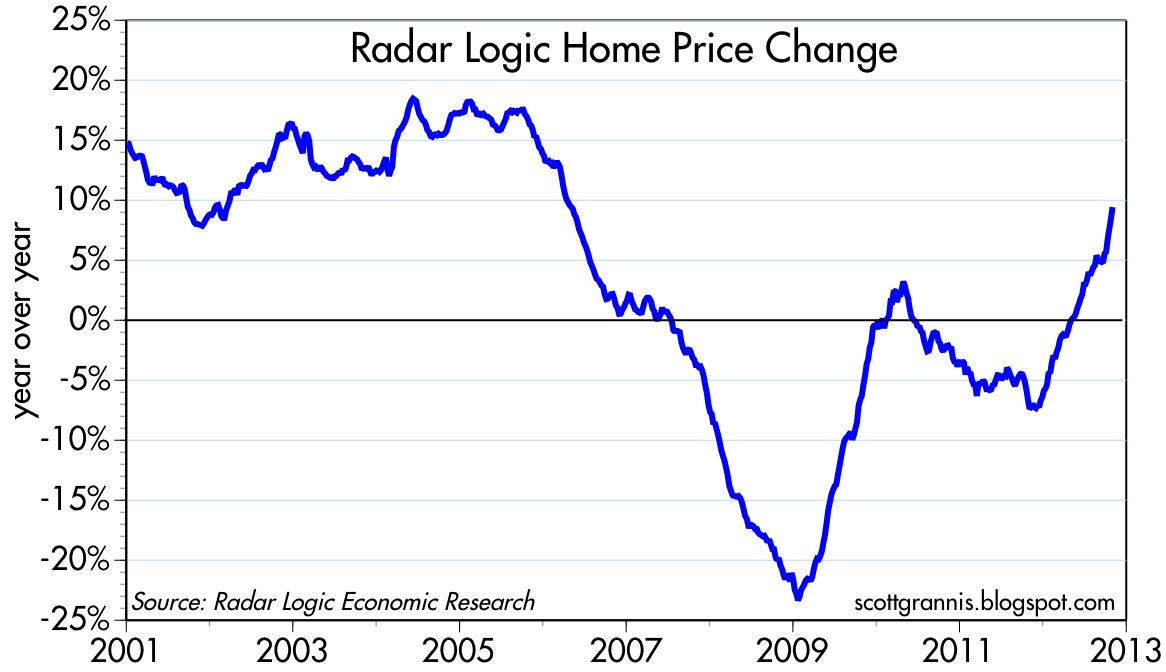

Housing starts were so low for so long that the housing stock shrunk significantly relative to demand. As this chart shows, housing prices are up almost 10% in the past year. Demand and supply have come back into balance, and demand—fueled by the lowest mortgage rates in history and abundant cash—threatens to push prices higher still.

These are all impressive charts, but this last is the most impressive of all. Thanks to three rounds of Quantitative Easing, the Federal Reserve has purchased a net $1.5 trillion of MBS and Treasuries, and has created a similar amount of bank reserves in the process. Almost all of the increase in reserves is still sitting idle at the Fed, which means that banks are content to hold a huge portion of their balance sheets in reserves paying only 0.25%. As is the case with consumers who love savings deposits for their safety rather than their yield, this reflects a banking system that is still very risk averse. Should that change, however, and should banks become more willing to lend, they have an almost unlimited potential to do so. If the Fed fails to manage this huge excess mountain of reserves properly, it could quickly turn into an Everest of extra liquidity washing through the economy, boosting growth and boosting prices in the process.

All of this bears close attention, since it runs directly counter to the popular meme that the U.S. economy is struggling and possibly on the verge of another recession. Where there's a lot of smoke, as these charts show, there is bound to be some unexpected fire.

As a supply sider, I am as gloomy as anyone when it comes to the outlook for the economy at this juncture. The fiscal cliff deal will cause taxes to rise on almost everyone, especially risk-takers and small businesses, and that adds up to a drag on growth. Regulatory burdens and costs associated with the implementation of Obamacare are just beginning to have an impact, with much more to come. Higher taxes are in effect validating a higher level of government spending, and that reduces the economy's overall efficiency, and that in turn translates into slower growth than could otherwise be possible.

But when I look at these charts and realize the enormous changes that are occurring beneath the surface of what most believe is a very sluggish and calm economy, I come away thinking that optimism is more likely to be rewarded than pessimism, even though the drumbeat of news is depressing.

FED RESERVES WILL ALWAYS BE FED RESERVES REGARDLESS OF LENDING OR NOT BY BANKS. THEY REFLECT THE SUBSTITUTION OF MONEY FOR ASSETS. THEY MUST REMAIN ON THE BOOKS UNTIL THE FED RETIRES IT THROUGH ASSET SALES. HOW COULD YOU NOT KNOW THIS? IT RENDERS ALL YOUR WRITING SUSPECT.

ReplyDeleteYour criticism is entirely unfounded. Apparently you did not read my post last month "The Fed leverages up," in which I noted that

ReplyDelete"bank reserves are not cash and they can't be spent anywhere: like pajamas, they are only for use "in house," since they are always kept at the Fed. Bank reserves do have a unique feature, of course, that other short-term assets don't: they can be used by banks to create new money, and in fact, acquiring more reserves is the only way that banks can increase their lending, because banks need reserves to back their deposits. Since banks now hold $1.6 trillion of reserves, of which only $0.1 trillion is required to back current deposits, banks already have an almost unlimited ability to make new loans and thereby expand the money supply. A year from now they will have an even more unlimited ability to do so."

Someone got his CAPS LOCK stuck...

ReplyDeleteScott, you forgot one chart that really looks fantastic: government debt, or better, government debt including unfunded liabilities.

Wonder how all the other charts would looks like without debt increasing much faster than GDP?

Nice wrap up.

ReplyDeleteI think the Fed is doing the right thing, and that is (honestly) printing money and buying bonds, thus shoving lots of cash into the economy. I just with the Fed had started to do tho earlier and heavier.

Can the USa escape the zero-bound, perma-recession of Japan?

We know fiscal deficits do not work; see Japan.

It is up to the Fed.

And we know from Japan if a central bank places priority on fighting inflation, when the economy is on zero bound, then you get perma-zero-bound-recession.

Bernanke is aware of this; John Taylor is aware of this; Milton Friedman was especially aware of this.

O totally agree with Scott Grannis on the shameful increase in structural impediments---ethanol, higher taxes, Obamacare, a runaway Pentagan, VA, and Homeland Security apparatus, and a wantonly subsidized rural America.

Add on lengthy unemployment benefits.

you just don't get it. a loan then cycles through to another bank's reserves. the reserve amount stays the same regarless of loans. reserves don't constrain loans, capital does.

ReplyDeleteThat's precisely my point. Reserves are no longer a constraint on bank lending, and obviously a lot of banks' capital is tied up in reserves. Bank lending is only restrained by banks' willingness to lend. If they become more confident they can lend massively.

ReplyDeleteScott, thanks for your blog and commentary. I am having a hard time understanding government debt fundamentals (im sure we all are!) the total debt number is 15ish trillion, is that the market value or face value? (Inflated treasury bonds?). Could the government borrow another trillion from china and invest it in equity in China. They lend us money and we buy them? Could the fed just print 15trillion new dollar bills and pay off every body that has a treasury debt?( this would cause inflation but at least we wouldnt have debt? Could we sell all of the national parks and government buildings to pay off the debt? How can the fed best use its balance sheet for long term prosperity? Could we sell our current bonds at rediculously high prices to european or asain governments and pay off debt or invest in equities. Or maybe wise american investors are already doing this. Nothing about the government and the debt and spending makes any sense right now to me i am confused, thanks for trying to help!

ReplyDeleteMaybe it would help to peak into a lending department inside a bank once. Banks don't lend because their CEO (or underlings) become "more confident". It's debt-to-income ratios, loan-to-value, underwriting standards, capital requirements.

ReplyDeleteIf households are over-leveraged they need to de-lever. Neither excess reserves nor "confidence" make a difference.

you said this in the referenced post: "Almost all of the increase in reserves is still sitting idle at the Fed, which means that banks are content to hold a huge portion of their balance sheets in reserves paying only 0.25%. As is the case with consumers who love savings deposits for their safety rather than their yield, this reflects a banking system that is still very risk averse." this is completely wrong. no matter if they lend it or not, the amount of reserves won't change. you misapprehend reserves and captial. they are excess reserves b/c they represent the issue of money for assets. if the bank "loan out the reserves" (which it doesn't do anyway) they reserves would end up right back at another bank with fed account.

ReplyDeleteThe reserve account of a bank at the Fed is a demand deposit with no restrictions on it, except to maintain a required minimum balance. The excess over the required reserves can be used at any time in any way. The bank may and does buy more treasuries and agencies to replace the ones that the Fed purchased, purchase physical oil for later delivery, and buy corporate equities that it intends to sell to an insurance company later. The bank couldn’t do that without having that thing called reserves that actually becomes money when it is spend, lent, or invested into the economy.

ReplyDeleteIn aggregate, the reduction of money in one bank’s reserve account is offset by an increase in another bank’s reserve account, who was the beneficiary of the money spent, lent, or invested by the first bank. That original spend ended up in another bank as deposits which are then kept at the Fed. So reserves don’t increase or decrease by spending, lending or investing. But there sure was a lot of economic activity, a good kind or a bad kind, from the increased money supply.

Interesting write-up by Lee Adler today, sort-of on the same topic:

ReplyDeletehttp://www.businessinsider.com/banks-not-lending-2013-1

Scott

ReplyDeleteI have read a few articles on the fiscal cliff deal that state the ratio of spending cuts to tax increases is something on the order of $1 to $42. Is this ratio accurate? Thx.

Happy New Year!

It may be accurate, but I haven't looked closely at the numbers. It may be entirely wrong also, since I believe that the CBO estimated that the net effect of the "deal" will be to increase federal borrowing by some $330 billion.

ReplyDeleteIn any case, I seriously doubt whether the spending cuts are significant, and I doubt whether they will ever take effect. Moreover, "cuts" does not mean actual reductions in spending, but rather spending that is less than the baseline.

Re housing; "Demand and supply have come back into balance".

ReplyDeleteThey always were in balance. Just at a lower price and higher level of inventory.