Inflation expectations are rising. This chart shows the Fed's favorite forward-looking indicator of the market's inflation expectations (the 5-yr, 5-yr forward expected inflation rate embedded in TIPS and Treasury prices). In September of last year, this measure of inflation expectations was a relatively mild 2.0%. Today, it has climbed to almost 2.8%. This is by no means a big concern, since 2.8% inflation is only slightly more than the 2.4% annualized increase in the CPI over the last 10 years. But it does show the bond market is becoming a bit uneasy about the prospects for future inflation. More Fed ease at this point would be hard to justify.

The dollar is weak vis a vis other currencies. This chart shows the Fed's calculation of the dollar's inflation-adjusted value relative to a large basket of trade-weighted currencies and a smaller basket of major currencies. No matter how you look at it, the dollar is trading only slightly higher than it's all-time lows. More Fed ease could weaken the dollar further, and a weak currency tends to exacerbate inflationary pressures.

There is no shortage of money. The M2 measure of money is growing above its long-term, 6% annualized growth rate. Most of the extra growth has come from savings deposits, which now total $6.4 trillion, up from $4 trillion four years ago. For now, it's obvious that there is a tremendous demand for safe dollar liquidity, but should this change, a flood of money could be released from savings deposits into the economy in the form of extra spending. And of course, the Fed has already been extraordinarily generous in its provision of reserves to the banking system. For now that appears to have been justified by the world's voracious demand for dollar liquidity and safe dollar assets (bank reserves now function as a close substitute for 3-mo. T-bills). But that could change, and if the Fed fails to withdraw the reserves in timely fashion, it could support a massive amount of new money creation.

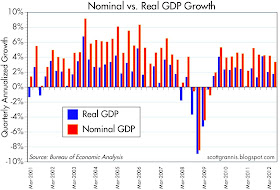

The economy is still growing, albeit at a modest pace. Since the recovery began three years ago, nominal growth has averaged about 4% a year. It dipped only slightly from that level in the past year. Real growth has averaged about 2%, and it too dipped only slightly in the past year. Jobs continue to expand, and new claims for unemployment are relatively low and stable. Thus, there are no signs that growth is slowing further.

UPDATE: In view of the above, it is not surprising that, while Bernanke left the door open to further easing measures in his Jackson Hole speech today, he made no promises. If the economy deteriorates then the Fed will do something. But for now, there is no sign of deterioration, just disappointingly slow growth. As Bernanke also said, it's the turn of fiscal policy to make a difference.

I think that he should say that in order to reward saving / savers, the FED will raise the funds rate by 1/4% to 1/2%.

ReplyDeleteThis 1/4% salve to the US banking system and to the US Treasury debt auctions has gone too long.

Thankfully, corporations live in the world of nominal growth so 4% plus productivity growth of 1.5 to 2.5% provides a vastly better return than cash, money markets and all bonds, except high yields.

ReplyDeleteThat was surprising expected inflation data in your Bloomberg chart. St. Louis Fed series DFII5 from the 5 year TIPS is at -1.26 and DGS5 from the 5 year Treasury is at 0.69, leaving a spread of 1.95 as of Aug 29, 2012.

ReplyDeleteBrian: the spread you refer to is a measure of inflation expectations over the next 5 years. The spread I refer to is a measure of inflation expectations over the five year period beginning 5 years from now.

ReplyDeleteWhen Bernake says that the FRB will take extraordinary steps if needed we have to remember that they already have taken some like buying long term govt's. The only things more extraordinary left to them, it seems, is corporate bonds and common stocks. It is this later strategy that I think the FRB is alluding to; the FRB will be buying common stocks not unlike what the Chinese did in 1997-98. If the FRB takes this step the country will have been taken over by a handful of people, a disgusting possibility. What in the world are we coming to?

ReplyDelete