Let's start with swap spreads, excellent and leading indicators of systemic risk. This chart shows that the U.S. first decoupled from the Eurozone in mid-2009, as U.S. swap spreads fell while Eurozone swap spreads rose. We got a hint of contagion in the second quarter of 2010 when all swap spreads spiked (in response to the first eruption of sovereign default risk), but U.S. spreads quickly settled back down. We saw another hint of contagion in the second half of last year, as the Greece default disease reached its climax, but once again the U.S. fundamentals improved even as Eurozone conditions remained fragile. U.S. swap spreads are still firmly within a "normal" range, but Eurozone swap spreads are still quite elevated. The Eurozone has avoided a financial meltdown—thanks to aggressive easing by the ECB—but default risk remains high because too many countries in the Eurozone have bloated governments that are strongly resisting the need to go on a diet. Capital flight, the risk of increased tax burdens, and fears of a Euro breakup have weighed heavily on European economies.

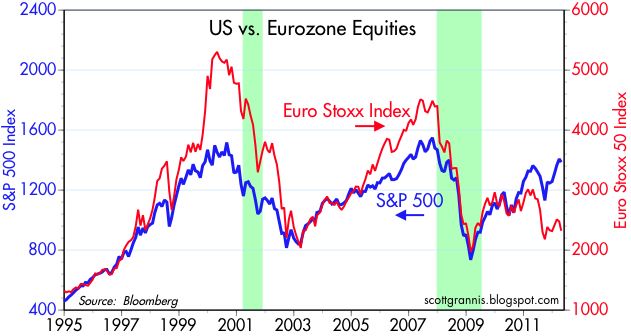

Comparing the performance of U.S. and Eurozone equities (above chart), we see that the true decoupling of the U.S. and the Eurozone began in 2010, as U.S. equities marched irregularly higher, while Eurozone equities marched irregularly lower.

The chart above shows the ratio of U.S. equities to Eurozone equities. Since early September 2010, U.S. equities have outperformed their Eurozone counterparts by over 50%. That's a pretty solid indicator of just how immune the U.S. economy has been to catching the Eurozone flu. It's actually very impressive.

To be fair, I should acknowledge that the U.S. has benefited significantly from the dollar's reserve status: with the future of the Euro in doubt, the dollar becomes the default currency for just about anyone seeking a safe haven these days. The U.S. economy has indeed benefited from significant capital inflows from Europe, as the above chart suggests.

Moreover, even though the U.S. fiscal picture is not much better than the Eurozone's in aggregate (all major economies have a severe over-spending problem it seems), the size of our federal debt does not necessarily pose a risk to the dollar, just as Japan's monstrous government debt has not hurt the yen. The same cannot be said for the Eurozone, since national governments there are not free to inflate or devalue their way out of their debt morass, leaving a breakup of the euro as one viable—but not very attractive—option.

The U.S. has one more thing going in its favor right now, and that is the growing likelihood that the November elections will reveal that country is getting serious about attacking its deficits. We have already benefited from a major shift in the balance of power in Congress, and now a change in the presidency looms. To make the point clear: Obama's recent budget proposal called for increased spending, higher taxes, and trillion dollar deficits for years to come, but not a single House Democrat was willing to vote for it. Obama and Harry Reid in the Senate are among the shrinking number of Washington politicians who still believe that the way out of our current mess is to spend and tax even more. Knock one or both of them out and the balance of power in Washington and the thrust of fiscal policy can change dramatically.

One important caveat: there is a good way and a bad way to practice fiscal austerity. Europe so far has been attempting to pare deficits through a combination of tax hikes and spending cuts, but this does not inspire confidence: tax hikes in the midst of a recession are not only politically difficult to implement, they can aggravate the weakness (the U.K. has already abandoned its attempt to boost taxes on the wealthy because it failed utterly to produce higher revenues) and that creates a negative feedback loop that can push deficits even higher. The U.S. is toying with tax hikes, but I don't seen any meaningful chance of that happening. It's far more likely that the U.S. federal deficit will continue to decline relative to GDP (as it has for almost two years now) thanks to spending restraint and continued moderate growth. If the U.S. can achieve some significant tax reform (e.g., broadening the base by eliminating loopholes, deductions, and tax subsidies, in exchange for lowering marginal tax rates, plus cutting the corporate tax rate meaningfully), then the resulting stronger growth could do wonders for deficit reduction.

Another refreshing wind of change blowing through Washington these days is the growing perception that government spending does not stimulate an economy, and can in fact weaken an economy. Keynesian theory has suffered what could prove to be a fatal blow with the failure of the Obama stimulus to boost the economy as advertised. If enough politicians come around to the realization that cutting spending (or at least not increasing it) can prove beneficial for growth, then "austerity" becomes a good thing. I'm not holding my breath for a development like this anytime soon, but I think that on the margin we are moving in that direction. And markets are always very sensitive to change on the margin.

Greece, Spain and Italy ought to leave the Eurozone and start printing money. They are detained for very long-term recessions, otherwise. They also ought to balance their budgets.

ReplyDeleteI see no hope for Europe. Too much taxed, too much regulation, and tight money. A toxic combination.

The USA is doing a Japan--our only hope is that Romney wins, and the Chicken Inflation Littles switch sides and call for a bullish Fed now that the GOP is in the White House. That happened when Reagan was President.

Reagan ran big deficits and so will Romney, as the Bush-Bush era mantra "deficits don't matter" will re-emerge.

The future is in Asia.

Recommendations to speed recovery with inflationary policy are a consequence of too many pundits and economists too quickly attempting to compare the crisis to the Great Depression. While there should be concern that such an event never happen again, attention should also be focused on policies that will prevent a return of the stagflation the 1970s and 1980s. The "Great Moderation," a nearly 20-year period of economic growth and low inflation, made it appear that policy makers had learned the lessons from policy errors made between 1960 and 1980. A shift in monetary policy emphasis from high employment to price stability — which even Hayek argued might be the best policy to be expected from a central-bank-headed fiat-money regime — appeared until 2000 to be successful. Two Austrian-style boom-bust periods ended the appearance of macroeconomic tranquility.

ReplyDeleteThe first boom-bust, circa 1995–2000, provided evidence that, per Hayek in the 1930s (sounding much like Krugman now), "price stability isn't an adequate guideline for monetary policy." The reason, contra Krugman, is that a monetary shock that accommodates a productivity shock generates a boom. For this period, this is illustrated by real GDP above potential GDP. The resulting "bust," at least measured in terms of the cycle impact on GDP, was relatively mild.

However, the mild recession was followed by a relatively slow, jobless recovery. This led many economists, including Krugman and pundits, as is now happening, to encourage the Fed to reinflate — create another boom or bubble — to ignite growth and employment. Thus the Fed turned to monetary excess. Interest rates were kept too low for too long, which led to "a boom and an inevitable bust" (Taylor, 2008, emphasis mine). This housing-bubble-led boom-bust is an excellent example of Hayek's and ([1939b] 1975) and Ravier's (2011) misdirection of production that results from monetary stimulus of an economy currently operating below potential. This monetary policy, designed to reduce unemployment in the short run, became a cause of "more unemployment than the amount it was originally designed to prevent" (Hayek, 1979, p. 11 and Ravier 2010, especially Grafico IV, p. 116).

$10.00 $5.00

More inflation now would just repeat the mistake, trading some lower unemployment now for more unemployment and more inflation in the future. To avoid holding a tiger by the tail avoid inflation now. The crisis and slow recovery should not be an excuse to revive failed Keynesian policies but instead to examine critically a denationalization of money.

Scott, you say, "The U.S. is toying with tax hikes, but I don't see any meaningful chance of that happening."

ReplyDeleteBut you have forgotten about Taxmaggedon! Which arrives promptly on January 1, 2013. If Obama/Congress do nothing a huge tax hike is already scheduled to go into effect to the tune of $500 billion!

Obama is toying with more—and I agree that I don't see that happening. But the Bush tax cuts will end:

Odds Obama/Congress fix this before then? 1%. Not going to happen. Obama extended them once, he has upped his rhetoric against the rich significantly since then. He won't do it again.

Odds Romney/Congress fix this after then? 20% May happen, but doubt the Senate will go conservative enough to get to the 60 votes needed.

That means I have an 80% chance of seeing my tax rate almost triple (I have no earned income). I would say that is meaningful!

I think I overstated my case on the risk of tax hikes. But even though there are some huge tax hikes scheduled to take place next year, I don't think any member of congress wants to risk allowing that to happen with the elections in sight. A huge tax hike would be very bad for the economy as it stands today (still pretty weak). Someone (likely a Republican) will make the case for extending the cuts, and very few will want to vote against that. The election will in effect be a referendum on whether we should raise taxes or not. We should let the elections decide.

ReplyDeleteWill not a recession in Euroland become ours?

ReplyDeleteScott,

ReplyDeleteWhen you advocate for "broadening" the tax base, does this in general mean that the tax burden is shifted down the cohorts of income earning households? If so, what is your view on those households' ability to pay taxes and also maintain some desired level of spending?

I am just trying to se how people who now pay little to none in taxes under our current system - other than FICA, that is - will afford to pay more.

Re broadening the tax base. There are many dynamic consequences involved here. Ideally this would mean eliminating all deductions and loopholes, in exchange for much lower tax rates. Many income earners in the bottom half of the income scale would pay very little or nothing, but more people would be paying at least something. I think it's important for the majority of workers to pay at least some income tax so they have some skin in the game. Lower marginal rates would be a boon to a great majority of workers, since additional income would be taxed at a much lower rate. This would make it easier for people to climb the prosperity ladder, whereas now marginal tax rates can be extremely steep between 70K and 175K of income. A lower corporate tax rate would mean lower prices for many goods and services (the burden of corporate taxes fall mainly on consumers). Lower tax rates would increase everyone's incentive to work and invest, and reduce the incentive to seek tax avoidance. A simpler tax code would reduce compliance costs dramatically (no need for all those CPAs and tax attorneys). Some would pay more, but most would be better off.

ReplyDeleteGuys, with all due respect, you're missing the big picture. It's all about oil (and alternatives to foreign oil, i.e., domestic nat gas) and health care. Nothing's fixed until they're fixed.

ReplyDeleteTaxes shmaxes.