This is perhaps the most popular measure of the dollar's value, and it compares the dollar to the Euro, Yen, Pound, Canadian Dollar, Swedish Krona, and Swiss Franc on a trade-weighted basis. The dollar by this measure is up 1.5% for the year, but that is small consolation given how weak it remains.

This second chart compares the dollar to a very large basket of currencies on a trade-weighted basis. Pretty much the same story as the first chart: the dollar is very weak.

The third chart (arguably the best measure of the dollar's overall value against other currencies, and my personal favorite) compares the dollar to a very large basket of trade-weighted currencies, and is adjusted for inflation differentials. This corrects for those situations where high-inflation currencies fall by a lot against the dollar in nominal terms; if not corrected for inflation differentials, the effective decline in those currencies is exaggerated, and thus the dollar comes out looking stronger than it really is. This index shows the dollar has—for the fourth time since 1973—hit an all-time low.

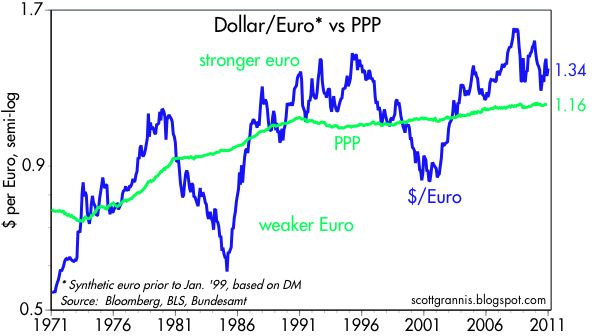

This next chart (above) shows the dollar vs. the euro, using a synthetic value of the euro (based on the DM) for the years prior to 1999. In this and in the charts that follow, the green line is my estimate of the purchasing power parity (PPP) of the dollar—the exchange rate that would equate prices between the two countries. This value changes according to relative inflation differentials. In the case of the euro, the PPP value of the euro has been trending stronger since the 1970s because inflation in Europe has for the most part been lower than inflation in the U.S. According to this chart, at today's value of 1.34 dollars per euro, the euro is about 15% "overvalued" against the dollar. That is a way of saying that a U.S. citizen traveling in Europe is likely to find that, on average, things cost about 15% more in Europe than they do in the U.S. Note that the dollar has been much weaker against the euro than it is today, and the reason for this is that the euro is suffering from fears that sovereign defaults among its member nations (e.g., Ireland, Portugal, Spain, and Italy) could result in a breakup of the euro. Personally, I think that is a very unlikely event, but in the meantime the perceived threat to the euro ends up being to the advantage of the dollar.

This chart (above) shows the dramatic gain in the value of the Canadian dollar vs. the US dollar. Relative to its PPP, the loonie today is almost as strong as it has ever been. US tourists are likely to find that traveling in Canada is quite expensive these days. Strong commodity prices have helped support the loonie, as has its central bank. Monetary policy in Canada has been less volatile than in the U.S., and Canada has apparently avoided a housing and bank bust.

The Australian dollar (above) has also benefited enormously from strong commodity prices, which in turn have boosted its resource-based economy, with the result that it is now about 50% "overvalued" relative to the dollar by my calculations.

The pound at $1.56 is only about 12% "overvalued" by my calculations, and it has weakened considerably in recent years. (I was unlucky to have my daughter studying in London during the years when the pound was the strongest.) The long-term trend of the pound against the dollar has been down, and that is explained by the fact that inflation in the U.K. has been consistently higher than in the U.S.

I note that all of these major currencies are "overvalued" relative to the U.S. to some degree. That's the flip side of saying that the dollar is "undervalued" against all these currencies, and that confirms the message in the first set of charts above, which is that the dollar is generally very weak.

This last chart compares the dollar (blue line, inverted) against one measure of commodity prices. Note how the correlation between the two has been fairly strong in the past decade—dollar weakness corresponds to commodity strength, and vice versa. This is one way of showing that there is a monetary explanation for rising commodity prices: a weaker dollar buys less of other currencies and fewer commodities. Dollar weakness, in turn, is ultimately the responsibility of the Fed: keeping interest rates too low results in an effective over-supply of dollars, and a loss of the dollar's purchasing power.

Bottom line: the dollar is unequivocally weak against many objective standards (e.g., gold, commodities, and other currencies). It's about as weak, in fact, as it has ever been, and its prospects are grim, since the Fed has vowed to remain ultra-accommodative for a long time to come. If there is a silver lining to this dark dollar cloud, it is that with the dollar at extremely weak levels, perhaps all the bad news is priced in. If so, then the dollar becomes quite "vulnerable" to any good news, or simply to a failure of the expected bad news to show up. I'm on record as predicting the dollar will strengthen against most major currencies this coming year, and I sure hope I'm right, since further dollar weakness from this point would be very unpleasant, if not inflationary.

Scott,

ReplyDeleteA happy and prosperous new year to you and your family.

To all commenters on Scott's blog, I wish the same.

Happy New Year!!

Inflation, schmaflation.

ReplyDeleteThe weak dollar boost exports, and that boost GDP.

The dollar is "weak"-- I say the dollar is at a "trade-enhancing level--for two years, and where is the inflation?

Indeed, we have had disinflation for the last two years, and may be moving towards deflation. Some in the Fed are predicting zero inflation next year, a sentiment I agree with.

A prosperous New Year to Scott, John and all readers also!

If you want low inflation, move to Japan. Their economy has grown by 15 percent in the last 20 years, whole ours has grown by 150 percent.

If a central bank has one goal--price stability--the economy will suffer badly. That is the lesson of Japan.

The dollar is very weak, and the cost of restoring the dollar's strength would essentially require that Americans give up all public services (public education, social security, and Medicare only would be a downpayment) with a concomitant doubling of taxes to pay off the national debt. Oh, and the winners of repairing the dollar would not be anyone in the 99% club. Let me think -- I have only one lifetime. We should all hope for inflation...

ReplyDeleteexcellent post. i am amazed you would write this and the prior post and not see the direct connection with dollar debasement and nominal asset prices. the money illusion indeed.

ReplyDeleteYou are right, the USD is weak, or are those other currencies overvalued?

ReplyDeleteCan't speak for other currencies but as a Canadian I know the loonie probably is, the PPP tells you that but you must also know that if Canada did managed to do relatively well during the crisis it did so at the cost of an unprecedented growth in household debt (the housing bubble grew even DURING the recession...). The real estate market in particular is supported directly by the federal gouvernement (taxpayers) via the CMHC which is the totally public Canadian version of Freddie/Fannie.

As a result houses are now roughly twice more expensive in Canada than the US and household indebtment has now surpassed the US. Although public deficits are (for now) smaller the public debt is also larger then the US and the fiscal margin is much thinner. As a whole Canada is one of the most indebted nations in the world. You have to wonder what will happen when the debt binge stops...

In short Canada's presumed strength which is still reflected in its currency might just be an illusion and the USD weakness an opportunity!!!

Happy new year everyone!

Jean-Pierre: You are absolutely right. When currencies reach valuation extremes, as is the case with the dollar (very cheap) and the loonie (very expensive), then they become vulnerable if conditions and/or sentiment change.

ReplyDeleteA pretty girl at a financial paper I worked at once asked, "How come all the currencies are going up except the dollar?"

ReplyDeleteScott,

ReplyDeleteIf your 2011 predictions are correct, and the Fed hikes sooner than expected, and the dollar strengthens, I would expect commodities to suffer and emerging market equities to pull back. We saw this will the small bursts of dollar strength in 2010 around the European default scares. Your predictions seem to call for dollar strength but ignore the impact on commodities and emerging market stocks.

REW: You have a good point. An earlier-than-expected Fed tightening would likely be bad for gold, commodities, and emerging markets, and I wouldn't be surprised to see them suffer a nasty selloff should that happen. But it's hard to see how the Fed could tighten enough this year to really make a difference to the fundamentals. Even if they raised the funds rate to 1.0% (three tightenings), monetary policy would still be very accommodative, and thus supportive of these markets.

ReplyDelete