Two weeks ago I highlighted the spike in swap spreads both here and in Europe, noting that they indicated deep-seated fears of banking risk in Europe, and the possibilty that this could end up tipping the U.S. economy into a double-dip recession. Europe is still in the grips of that fear, as 2-yr swap spreads hover around 80 bps, with 30-40 being a more normal level. (The main driver of wider spreads in Europe is an unprecedented—for Europe—flight to quality, as evidenced by plunging yields on German government debt: 2-yr German govvies now yield a mere 0.5%, while 10-yr Bund yields have fallen to 2.5%, by far the lowest level I can recall.) But U.S. markets have become much less concerned about banking risk, since 2-yr swap spreads have backed off to just over 40 bps, which happens to be equal to their 20-year average, and OIS spreads (overnight swap rates minus 3-mo. T-bill rates) are only marginally higher than average.

This next chart collects the three major indicators of market fear and uncertainty in the U.S. A few things stand out. For one, the current fear episode is much less severe than the panic of late 2008. Two, fear is concentrated in the equity market; the Vix index has backed off its recent highs, but is still significantly higher than average and well above "normal" levels of 10-15.

Putting all the pieces together, these market-based indicators are telling us that the U.S. market's main concern is with the possibility of a double-dip recession, which in turn might be triggered by a banking crisis in Europe. It's very hard to find However, most of that fear is based on events that have not yet happened. To date there have been no signs of a developing recession in the U.S. or in Europe, and there have been no defaults yet in Europe. Commodity prices are down from their recent highs, but not by nearly enough to warrant the conclusion that global demand is shutting down.

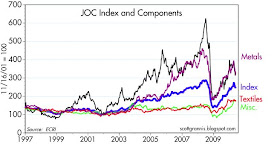

I wouldn't be surprised to learn that the unusually wide spreads and the general sense of a banking panic in Europe are being driven more by speculation than by fundamentals. For example, note in the above chart that it is industrial metals and petroleum products (which can be driven by commodity speculation) that have moved the most—both up and down—whereas the more obscure commodities (e.g., cotton, burlap, polyester, hides, rubber, tallow, plywood, and red oak) that are in the Textile and Misc. subindices of the Journal of Commerce Index are still trending higher. Speculators, fresh from studying how the 2008 banking crisis and economic collapse in the U.S. unfolded, are surely eager to profit from a what they expect will be a similar chain of events in Europe.

Speculative attacks can be self-fulfilling prophecies, of course, but in this case they are occurring against a backdrop of strength (global recovery in demand, rising production, accommodative monetary policies), whereas in 2008 the panic grew out of the unravelling of the housing market and its myriad derivative securities that was several years in the making, and it all reached a climax with the government's fatal mishandling of Lehman. Spreads soared—both here and in Europe—because people were running for the exits. Spending collapsed because of fears of a global banking collapse, and because many borrowers were unable to fund themselves and/or were forced to sell positions at firesale prices. The problem in Europe is much less broad, involving only a handful of borrowers and vastly smaller sums of money. Perhaps spreads are wide at least in part because of speculative short-selling, rather than broad-based panic. In any event, as I've mentioned before, buying Greek CDS or otherwise betting on a banking or sovereign default is an expensive proposition, especially now that spreads are so wide. The more time passes without a default, the less interested speculators will be in holding positions which are currently costing anywhere from 250 to 800 bps per year. And since U.S. spreads are not nearly as wide as they are in Europe, the market is implying that the risk of contagion is much less this time around.

This may be unscientific of me, but I'm reluctant to buy into the fears of double-dip recession. If for no other reason, it seems there are just too many people running around predicting the collapse of Europe. A friend sent me a lengthy piece from BMO Capital Markets in Canada, with the title "Go to Cash — In Plain English." It points out all the things that could go wrong in Europe and recommends that investors sell ALL equity positions and hide out in cash, which by the way is paying virtually nothing. This is the kind of recommendation that will pay off only if disaster strikes. The last disaster caught nearly everyone unaware and unprepared, and that was a big reason it was so destructive; but we can hardly expect a widely-anticipated European banking crisis to be as bad.

Marc Chandler of Brown Brothers Harriman is reporting today that the Swiss Central Bank (SCB) has been a HUGE buyer of European sovereign debt in the last month. They have stepped up to the tune of something like 40B euros which is nearly the same amount as the ECB. They are using their powerful currency to aid the EU and the Euro currency. The fact that the Continent has been devastated by two wars in the last hundred years is not lost on them. They have a powerful incentive to see the EU survive and thrive and they are stepping up, big time. While not nearly as large as the ECB, the SCB has big league credentials in financial markets. I suspect ALL central banks (including China and Japan) are working together in this crisis. It is in No one's interests (except the speculators) to have Europe's economy collapse. The global financial authorities still have powerful cards to play.

ReplyDeleteThis comment has been removed by a blog administrator.

ReplyDeleteTexas Instruments (TXN-NYSE) is reporting this PM that their second quarter earnings will be at the upper end of their previously estimated guidance. VP Ron Slaymaker is quoted as saying "..we are seeing some pretty broad based strength..".

ReplyDeleteTXN is a manufacturer of analog semiconductor chips that go into a broad range of electronic products globally. Slaymaker also indicated orders from Europe were keeping pace with other regions.

This is from Bloomberg News.

Again, Europe may be facing a slowdown but it apparantly isn't happening yet.

There is a Washington Post article linked at the Realclearmarkets.com site that describes huge investments by China into Greece's shipping and port industries. The government has welcomed the investment and opposed the unions whose work rules increase costs. It appears the Chinese are continuing to buy when everyone else is running away.

ReplyDeleteMore evidence of global authorities playing strong cards in the Euro crisis.

Portugal has reportedly held a very successful bond auction at tighter spreads to the German bund.

ReplyDeleteChina's exports were greater than expected, indicating a strong global economy.

Way too much pessimism in our markets.

JMCO

Chairman Bernanke testified before the House Budget Committee this AM. For those of you who believe him to be credible it would be worthwhile to read his testimony.

ReplyDeletehttp://www.federalreserve.gov/newsevents/testimony/bernanke20100609.ahtm

For those who do not have the time or inclination, here are my brief takeaways:

1. US GDP +3 - 3.5%, somewhat higher next year (2011)

2. As stimulus subsides, private demand will sustain recovery.

3. unemployment will see "slow reduction over time"

4. Housing is experiencing modest improvement.

5. '..ongoing international cooperation...signal...WE WILL TAKE THE ACTIONS NECESSARY TO ENSURE STABILITY AND CONTINUED ECONOMIC RECOVERY' (emphasis is mine).

6. Our fiscal position is 'unsustainable'. PLAN NOW to correct (emphasis mine). We need a strong committment to fiscal responsibility.

The Chairman goes into more detail in the testimony but these are TO ME the most important bullet points.

I repeat, capitals for emphasis above are mine.

One other point: Regular readers of this blog should not see anything new in the above.

This comment has been removed by a blog administrator.

ReplyDelete