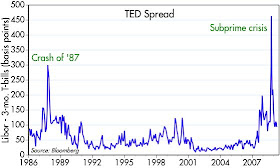

At the request of a loyal reader, here is an updated chart of the TED spread, which is very similar to the Libor/OIS spread he requested. I haven't posted this for awhile, mainly because it hasn't changed much so far this year, after collapsing in November and December. It's trading at about the same level today as it was in August '07. Still way above "normal," but well below the peak of late October '08.

At the request of a loyal reader, here is an updated chart of the TED spread, which is very similar to the Libor/OIS spread he requested. I haven't posted this for awhile, mainly because it hasn't changed much so far this year, after collapsing in November and December. It's trading at about the same level today as it was in August '07. Still way above "normal," but well below the peak of late October '08.It's probably too much to ask for this particular spread to fall back to normal levels at a time when the Fed is pursuing a quantitative easing policy. Fed policy has given us a short-term rate of almost zero, whereas 3-mo. Libor today is about 1.1%. The market is not expecting Libor to change materially until much later this year, when it is expected to be 1.4%. So we're at rock bottom, in a practical sense, for both of the spread components. I take that to be a positive, despite the fact that the spread is still unusually high.

Thanks!

ReplyDeleteThe current Contrary Investor commentary (a fee-based service) presents a good piece on credit market indicators. They show point by point that the Fed is manipulating all the credit market rates. They call it "fingers in the dike."

ReplyDeleteThere would be no apparent credit market healing without these Fed interventions, and there is no way we are going to get realistic "healing" until market prices are allowed to happen.

I think we are in for an interesting time if the Fed continues these multi-trillion dollar operations indefinitely -- and how can they stop?

These are very dangerous games these people are playing.

I know that the Fed is heavily involved in the markets these days, but I don't think they can control everything. As big as their balance sheet is, the Treasuries held by the world are much bigger. Mortgage-backed security holdings by the world are even bigger. The Fed can guide markets but it can't dictate prices for everything. Take the MOVE index, which is a composite of the implied volatilty of Treasury options. I don't see how they could be controlling that. It shows a gradual healing process underway, just as the VIX index does.

ReplyDeleteI certainly agree with that, Scott. But their involvement distorts all the credit market prices from what they would be without the interventions. The relative price (interest rates) distortions change human choices, which is what the Fed wants to do -- but they shouldn't. That behavior is going to bite them again.

ReplyDeleteAfter this horrendous housing bubble/bust now the Fed has a stated goal of getting mortgage rates down to 4%! These people are insane, in my humble opinion. Either that or they just think they can keep stealing trillions of dollars from dollar holders.

I agree that the Fed is making a mistake here, and they are really crazy if they think they can get mortgage rates down to 4%. Should that happen, though, I would be prepared to throw caution to the wind and buy at least a few properties.

ReplyDelete