(Just to be clear, as a supply-sider I think inflation should be as close to zero and as stable as possible. One way to do that, I believe, would be to return the U.S. to a gold standard or something similar that ties the dollar's value to an objective, physical standard. Central banking should not rest on the discretion or the judgment of a small group of (fallible) Wise Old Men, it should be about keeping the purchasing power of the dollar stable and predictable no matter what. The central banker of my dreams would be a person who firmly believed that the measure of his or her success would be directly proportional to how low and stable inflation proved to be, and inversely proportional to how much he or she had to work.)

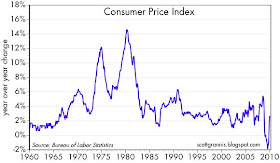

Inflation happens when there is too much money relative to the demand for it, but how do you know when there is too much money? As I've discussed before, there's no good measure of money supply, but there are good proxies for money demand. But without knowing money supply, how can you tell if it is exceeding money demand? The answer lies in the market-driven prices of the dollar, gold, commodities, T-bonds (i.e., the yield curve), breakeven spreads on TIPS, and credit spreads. What follows is a quick survey of what I think each of these prices is telling us about monetary policy and the outlook for inflation. If I were to replace Bernanke, these are the things that I would pay the most attention to.

Gold prices are close to an all-time high in nominal terms, but in today's dollars they are still shy of the $1800/oz high that occurred in early 1980 (note that the chart only plots year-end values). Gold prices are thus agreeing with the message of the dollar: there is a surplus of dollars in the world (but not nearly as much as there was in the late 1970s, thank goodness), and that makes investors nervous about the dollar's future purchasing power, which in turn leads to an increased demand for gold. Gold has the unique quality of being both monetary and physical, and its price has, over very long periods, tended to rise by the rate of inflation. If I had a chart of the real price of gold over various centuries, I think it would show that gold's price, in today's dollars, averages somewhere in the range of $400-500/oz. Thus, gold is correctly viewed to be the classic inflation hedge, with demand for gold rising and falling with inflation fears and fundamentals.

The two charts together show that the Fed almost always tightens policy as inflation rises, and eases policy as inflation falls. One major exception to this rule occurred in the 1995-2000 period, when the Fed tightened and the yield curve turned negative, yet inflation was flat or falling. I think this unwarranted tightening provides a very good explanation for why the U.S. economy was on the verge of deflation in the 2001-2003 period. Furthermore, the period of extreme Fed ease which followed was a key factor in driving commodity prices higher, the dollar lower, housing prices higher, and inflation higher over the 2003-2008 period.

The chart above shows the 5-year, 5-year forward breakeven spread on TIPS. That's the market's expectation of what the 5-year outlook for inflation will be five years from now. Not only have inflation expectations increased sharply in the past year, but the expected level of inflation (2.8%) now exceeds the average level of CPI inflation (2.6%) over the past 10 years.

Unfortunately there is a lack of good data on credit spreads going back in time, so I am forced to use this last chart to argue from a more intuitive basis. Credit spreads are the market's way of expressing default risk; the higher the spread, the greater the risk of default. Default risk is driven by a number of factors, but two important ones are the strength of the economy and the level of inflation. A strong economy typically leads to low credit spreads, since a healthy economy is good for corporate cash flows. A weak economy, in contrast, typically leads to rising spreads, since cash flows become uncertain and business bankruptcies almost always rise during and in the immediate aftermath of a recession.

Changing levels of inflation can also lead to changes in credit spreads. When inflation is high and rising, debtors are usually quite happy because their real cost of borrowing is low and they are able to raise their prices by more than they anticipated, which in turn means that their cash flows are stronger than expected. Rising inflation favors debtors to the disadvantage of creditors, so whne inflation rises investors are more willing to purchase corporate debt, and highly indebted issuers (i.e., junk bonds) benefit disproportionately. Thus, higher inflation typically contributes to lower credit spreads. Just the opposite is true when inflation is very low and/or when monetary policy is very tight, since it's difficult or impossible to raise prices, and the real cost of borrowing is very high. The best example of this was late 2008/early 2009, when inflation was sharply negative and many firms were forced to lower their prices; cash flows deteriorated and credit spreads shot up to unprecedented levels. Today, credit spreads are still high from an historical perspective, but the fact that they have plunged over the past year is one more piece of evidence that monetary policy is easy and inflation is returning.

Summary: All of these market-based indicators of inflation fundamentals are pointing in the same direction: higher. Meanwhile, traditional indicators of inflation that the Fed focuses on, such as the degree of economic slack and the unemployment rate, are pointing to very low or even negative inflation. Who's right? No one that I know has yet come up with a foolproof method or theory for predicting inflation, but I think it is reasonable to predict that inflation will be higher than the market expects (current expectations being for inflation to average 2-2.5% over the next 5-10 years).

This is an excellent set of graphs and commentary.

ReplyDeleteStill, I think we have a newish phenomena of "commedity investing" and commodity ETFs that we did not have before. I am also suspect of the NYMEX price.

Some speculators have become adept at selling "scare stories" about oil, lithium, copper shortages etc. You get a positive feedback loop of people going into ETFs, boosting demand for a commodity, raising the price, boosting demand etc. Not sure this is classic demand-pull inflation or classic commodity investing.

Huge pools of capital gush into any sector, based on PR, investment outlooks, fads.

Commodities are hot for now.

Before, it was real estate and China. Before that, stocks (they had a great 20-year run).

Gold is a cult unto itself.

Inflation under 3 percent for the next 10 years?

I can't say that strikes fear into my heart. In fact, I contend (sadly) that due to the inability of our major parties to balance the federal budget, we will need inflation to pay down the debt.

Let's get another boom going first before we worry about inflation.

Mr. Grannis:

ReplyDeleteIn your summary is mentioned the differing indicators/trends/direction of inflation.

The differing inflation indicators/trends/direction may very well be related to simultaneously deploying QE and Keynesian deficit government spending in a hyper debt environment.

The result being that the signals of inflation become distorted.

Thanks for the informative post and as others already mentioned great graphs. Showing my lack of depth, but is there away to translate the projected inflation rate of 2.8% (5-year, 5-year forward breakeven spread on TIPS Chart) into a projected 30 year treasury rate, or even a 5 or 10 year rate.

ReplyDeleteBenjamin: the market is saying inflation will be under 3% for the next 10 years. I'm saying it will probably be higher. The difference between 2% and 4% annual inflation can really add up. It's a big deal.

ReplyDeleteI'm sure there is speculation that is fueling the rise in some commodity prices. But the fact that virtually ALL commodities are rising tells me there is something more in the mix, like strong global growth.

Commodities may well be the next bubble. We'll have to watch closely.

I agree with you that will inflation may be a problem, the big news is growth which may surprise to the upside.

Scott and Fran: The short answer to your question is no. The market's implicit (breakeven) inflation rate is calculated using TIPS yields and yields on Treasury bonds. The Treasury yield is the given in the equation, not the result.

ReplyDeleteScott,

ReplyDeleteExcellent post. I wish your wish of a Fed chief and job tied to low to no + stable inflation materialized. And that the less work it took to achieve it, the better your compensation!

Sadly this will not happen. The only thing that will come from the past events is the Fed will tinker with its already flawed philosophy.

You can see it happening in real time with the debate over creating a "new" benchmark rate.

http://goo.gl/oDra

I agree with you inflation is here and peaking its head around the corner for just the right time to "surprise" everyone.

Thanks for the post.