Pessimism is rampant, and most of the articles and commentaries I see have some doom-and-gloom flavor to them; indeed, many pundits are already claiming to see a double-dip recession either in progress or as imminent. I think the "conservative" bull case—that the economy is growing at a sub-par trend rate of 3-4%, which will leave the unemployment rate uncomfortably high for some time to come—is not getting its fair share of the news. So here is my attempt to balance the scales: a collection of charts that to me point to ongoing economic growth, however mild that might be, with not a hint of a double-dip recession. All charts contain the latest data available, and they are shown in no particular order. I've discussed all of these in recent posts, so for long-time readers this just a recap of how I see things today.

Capital spending has grown at an impressive rate since the end of the recession, with no signs yet (assuming the July numbers contained a faulty seasonal adjustment, as I detailed in an earlier post today) of any slowdown. Strong capex reflects at least some positive degree of confidence on the part of businesses, and that is a leading indicator of future growth in the economy.

Industrial production is increasing at a very fast rate, with no signs of any slowdown. Most global economies also are experiencing a rapid recovery in industrial production. This is a good indication that the cutback in production that occurred in the wake of the financial crisis was sufficient to allow a substantial inventory drawdown. Now, with demand and confidence slowly returning, production must ramp up to avoid continued inventory drawdowns. Rising production supports increased confidence, leading to a virtuous cycle that all but guarantees further gains.

Commodity prices are up across the board. This likely reflects strong growth in global demand and/or accommodative monetary policies worldwide. Whatever the case, rising commodity prices all but preclude the deflation that so many are worried about, and rule out the existence of a double-dip recession.

Global trade is rebounding strongly. Rising exports are adding to U.S. GDP growth, while strongly rising imports reflect a healthy rebound in consumer demand, which in turn likely reflects a consumer that is in better shape than most give him/her credit for.

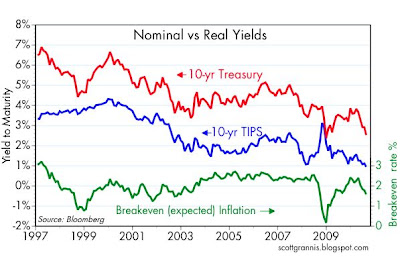

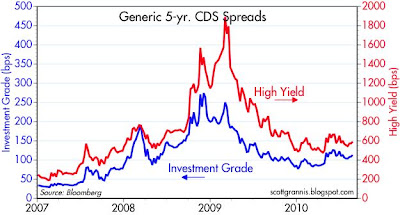

Credit spreads have been reliable leading indicators of recessions in the past. While it's true that spreads haven't tightened on balance over the course of this year, there is no sign of any rise in spreads that might foreshadow a return to recession. In any event, it's not unusual at all for several years to pass, following a recession, before spreads return to more normal levels. The behavior of spreads today—especially swap spreads, which are currently somewhat lower than what we typically see during periods of healthy growth—is fully consistent with an ongoing, albeit relatively sub-par, recovery.

The slope of the yield curve has been an excellent leading indicator of recessions and recoveries for many decades. The curve typically flattens or inverts in advance of recessions, but today it is still very far from being flat or inverted. The curve is strongly upward-sloping, which reflects easy money and expectations that monetary policy will eventually need to tighten as the economy improves. We've never seen a recession develop when the curve was this steep and monetary policy was this easy.

The fact that the demand for temporary and part-time workers is steadily increasing may not guarantee a continued recovery, but I think it argues strongly against a double-dip recession being underway.

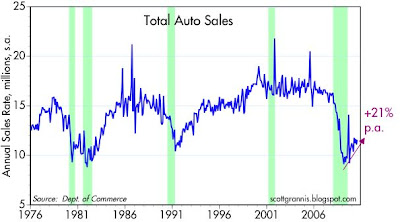

Car sales are up strongly over the past year, reflecting underlying improvement in confidence and in consumers' financial health. Car sales had fallen so much and for so long that this created pent-up demand that has the potential to be self-perpetuating. Bears focus on the fact that sales are still at abysmally low levels, but the correct way to see this is as very positive change on the margin.

Large corporate layoffs are essentially a thing of the past. It's very likely that corporations have done all or almost all of the cost-cutting that they need to do. A big decline in layoffs is almost a necessary precursor to a new wave of hiring, and that's what we're getting set up for.

China and almost all emerging market economies are growing like gangbusters, and global trade is recovering nicely. What's good for emerging market economies is good for everyone, since the more they produce the more they can buy from us.

Corporate profits typically decline in the years leading up to a recession, but for the past 18 months they have been growing strongly—which in turn is typical of the early years of a recovery. Strong profits are the fuel for future investments in new job creating ventures.

Although key indicators of financial health—most notably the Vix index, which at 27 is still significantly above its long-term average—are not in perfect shape, neither have they deteriorated enough to foreshadow any significant deterioration in the health of our financial markets.

Key indicators of shipping activity suggest that at the very least, there is no sign of any slowdown underway in global trade volumes or demand.

The Bloomberg index of the stocks of leading home builders hit a low almost 18 months ago and has more than doubled since. Prices of residential and commercial real estate have been flat to somewhat higher for more than a year. At the very least this tells us that the worst of the bad news from a housing and construction standpoint has passed. Residential construction is at an all-time low of about 2.5% of GDP, so even if things get worse, it would have only a modest impact on the overall economy.

It is arguable whether the Leading Indicators actually lead the economy, or whether they are just good coincident indicators of the economy. But in any case, they aren't even close to a level that would suggest that the economy has deteriorated to any meaningful extent. Indeed, they are at a level which strongly suggests continued growth.

Last but not least, I offer this chart which shows how the ISM manufacturing index has done a pretty good job of reflecting the underlying growth rate of the economy as a whole. Although the index doesn't match up exactly with each quarter's GDP growth rate, the recent level of the index strongly suggests that growth is still in positive territory, and that a 3-4% growth expectation for the current quarter is not unreasonable.